FHA mortgages have been a driving force in the housing industry offering affordable home financing for over five decades. Are you considering an FHA mortgage to buy your next home? If so, you probably have a lot of questions about the FHA loan process and what you need to do to be approved. It is important for perspective house buyers to know what the qualifications are to be approved for the best FHA loan. We created the ultimate FHA rate guide below, which explains the process to qualify for an FHA mortgage, so you know what to expect. This free guide will define the updated FHA home loan requirements and rules, so you understand what is needed to prequalify for an FHA loan at a competitive interest rate with the least amount of pain possible.

Compare FHA Mortgage Rates Today with Confidence

There have been some shifts in FHA mortgage interest rates. At the start of the current year, rates had held steady at under 6% for nearly half a year. However, the rates for 30-year mortgages began to climb and have continued their upward trajectory since.

The encouraging news is that potential mortgage rate shoppers seeking FHA loans might still secure fixed rates at affordable levels. FHA mortgages remain the top choice for individuals whose credit doesn’t meet the requirements for conventional loans. Even with a credit score in the lower 600s, it’s possible to secure a lower rate compared to conventional loans.

As the current FHA mortgage rates edge higher in response to economic improvement, being preapproved for FHA loans can be advantageous for securing a favorable deal.

While mortgage insurance costs are higher with FHA loans, the reduced interest rate often offsets this expense.

Regarding the outlook for FHA loan rates in the current year, most experts anticipate that they will hover around the high-5% range by year-end. Historically, both conventional and FHA mortgage rates have remained relatively low, given market conditions.

Therefore, if you are contemplating an FHA loan, the present moment is likely an opportune time to act. It’s anticipated that rates will experience an upturn once the effects of the recent tax cut fully materialize. Ask about the FHA 40 year loan that enables home buyers to secure low mortgage payments.

The RefiGuide will help you apply for FHA mortgage loans at a payment you can afford from a lender you trust. Below is more information about how to shop for the best FHA loan in today’s market.

Best FHA Mortgage Lenders in 2026 — Scored & Ranked with NMLS Numbers

Not all FHA-approved lenders are equal. The lenders below are evaluated across six criteria that matter most to FHA borrowers: minimum credit score accepted, FHA loan volume (a proxy for experience), current rate competitiveness, closing speed, down payment assistance availability, and overall borrower accessibility. NMLS numbers are verified from each lender’s official licensing disclosure as of March 2026 — always confirm your lender’s NMLS status at nmlsconsumeraccess.org before proceeding.

| Lender NMLS # | HQ |

Min. Credit Score (FHA) |

RefiGuide Score /10 |

FHA Volume Rank 2024 |

Est. FHA Rate Range Mar 2026 |

Avg. Close Time |

Best For / Key Differentiators |

|---|---|---|---|---|---|---|

| Pennymac NMLS #35953 Westlake Village, CA |

580 (500 w/ 10% down) |

9.6 | #1 FHA lender Scotsman Guide 2024 |

6.03%–6.35% | ~21 days | Best overall volume leader. #1 FHA lender by origination volume. Offers 1% rate buydown first year + $1,000 closing bonus on purchase loans. Primarily online/phone — no branch network. FHA, VA, USDA, conventional, and refinance. Transparent rate publishing. J.D. Power above-average servicer satisfaction. pennymac.com |

| Rocket Mortgage NMLS #3030 Detroit, MI |

580 (500 w/ 10% down) |

9.4 | #1 by total volume largest retail lender |

6.05%–6.40% | ~21 days (15 days faster than avg.) |

Best digital experience. Largest overall mortgage lender by volume. Fully online application; award-winning mobile app. FHA comprises ~20% of portfolio. Lender credits available. J.D. Power #1 customer satisfaction multiple years. Also servicer of large Mr. Cooper portfolio. Strong FHA streamline and cash-out refi capabilities. rocketmortgage.com |

| Freedom Mortgage NMLS #2767 Boca Raton, FL |

550 (some programs) |

9.2 | Top 5 FHA FHA/VA specialist |

6.03%–6.38% | ~25 days | Best for low-credit FHA borrowers. FHA and VA specialist — one of the largest government loan issuers of GNMA securities. Lowest publicly advertised credit floor for FHA among major lenders. Eagle Eye program monitors rates and auto-notifies borrowers when refinancing makes sense. Licensed all 50 states. Strong FHA streamline refi volume. freedommortgage.com |

| loanDepot NMLS #174457 Irvine, CA |

580 | 9.0 | Top 5 FHA homebuilder JVs |

6.05%–6.45% | ~21 days | Best for online + in-person hybrid. 200+ locations + digital app. Waives lender fees on future refinances (“Lifetime Guarantee”). Strong homebuilder joint ventures (new construction FHA). $4,500 cash back for first-time VA buyers; similar programs for FHA. Large FHA purchase volume especially in Sun Belt. loandepot.com |

| Guild Mortgage NMLS #3274 San Diego, CA |

540 (non-traditional credit accepted) |

9.0 | Top 10 FHA est. since 1960 |

6.08%–6.45% | ~25 days | Best for first-generation buyers & DPA programs. Accepts non-traditional credit (rent, utilities) — helpful for thin-file borrowers. Extensive down payment assistance partnerships. FHA 203(k) rehab loans strong. Branches in 49 states. 65-year track record. Strong relationships with local realtors. guildmortgage.com |

| New American Funding NMLS #6606 Tustin, CA |

500 (FHA; manual UW) |

8.9 | Top 15 FHA underserved focus |

6.03%–6.50% | ~14 days (advertised) |

Best for 500–580 credit scores. One of the few major lenders that consistently works with 500–579 scores via manual underwriting. Bilingual support (Spanish). 14-day close advertised. Strong minority homeownership focus. Retail lender — applies direct. FHA, VA, conventional, USDA, non-QM. newamericanfunding.com |

| Carrington Mortgage Services NMLS #2600 Orange, CA |

500 (FHA + Non-QM 550) |

8.7 | Mid-size FHA government + Non-QM |

6.10%–6.60% (Non-QM higher) |

~30 days | Best for severely credit-challenged borrowers. Accepts 500 for FHA; 550 for Non-QM Flexible Advantage. One of the only lenders offering both FHA and Non-QM under one roof — helps borrowers who need FHA but don’t quite qualify. Also handles bankruptcy and foreclosure seasoning situations. National. carringtonmortgage.com |

| Fairway Independent Mortgage NMLS #2289 Madison, WI |

580 | 8.8 | Top 10 FHA purchase specialist |

6.08%–6.48% | ~25 days | Best for in-person local service. Strong local loan officer network (most states). FHA, VA, USDA, renovation, physician loans. DPA program partnerships. Also handles insurance, title, and utility switching. Consistently top-10 FHA purchase lender. Nonprofit arms (Fairway Cares, American Warrior Initiative). fairwayindependentmc.com |

RefiGuide scores (out of 10) reflect a weighted composite across FHA loan volume, minimum credit score accessibility, estimated March 2026 rate competitiveness, closing speed, borrower support quality, and availability of DPA programs. Scores are RefiGuide editorial assessments — not sponsored or paid placements. Rate ranges are market estimates for FHA 30-yr fixed at 580+ credit, 3.5% down, primary residence as of March 2026; actual rates vary by credit score, loan amount, state, and daily market conditions. NMLS numbers verified from each lender’s official licensing disclosure page as of March 23, 2026. FHA volume rankings sourced from Scotsman Guide and The Truth About Mortgage (2024 origination data). Always verify NMLS status at nmlsconsumeraccess.org before applying.

How to Compare FHA Lenders — The 5 Numbers That Matter

When requesting quotes from multiple FHA lenders (always get at least three), compare these five figures side by side on the same day:

| What to Compare | Why It Matters | What to Ask the Lender |

|---|---|---|

| Interest Rate + APR | APR includes lender fees rolled in — more accurate than rate alone. On a $300K FHA loan, a 0.25% rate difference = ~$45/mo or ~$16,200 over 30 years. | “What is your APR today for a 30-yr FHA loan at my credit score and LTV?” |

| Upfront MIP | FHA charges 1.75% UFMIP on all loans — this is standard and not negotiable. On $300K loan = $5,250 rolled into loan. | “Can you show me the UFMIP on the Loan Estimate?” (Should be 1.75% — flag if different) |

| Annual MIP (monthly) | Currently 0.55%/yr for most FHA loans (15–30 yr, >90% LTV). On $300K = $138/mo. Paid for life of loan if down payment <10%. | “What is my annual MIP rate?” (Should be 0.55% for standard 30-yr loan — verify) |

| Origination / Lender Fees | Varies widely — some lenders charge 1–2% origination; others charge $0. On a $300K loan, 1% = $3,000 difference. | “What are your lender origination fees, and are there any discount points built into this rate?” |

| NMLS # + State License | Federal law requires lenders to disclose their NMLS number. Verifies licensing and allows you to check for disciplinary history before committing. | “What is your company NMLS number?” Then verify at nmlsconsumeraccess.org. |

2026 FHA Loan Limits — What You Can Borrow

FHA loan limits are set by HUD annually based on the FHFA conforming loan limit. Effective for all FHA case numbers assigned on or after January 1, 2026 (HUD Mortgagee Letter 2025-21), the new limits reflect a 3.26% increase from 2025, matching national home price appreciation per the FHFA Q3 2025 House Price Index.

| Area Type | 1-Unit (SFR) |

2-Unit (Duplex) |

3-Unit | 4-Unit | Coverage / Notes |

|---|---|---|---|---|---|

| Standard / Floor Most U.S. counties (low-cost) |

$541,287 | $693,050 | $837,700 | $1,041,125 | 65% of $832,750 conforming limit. Covers most affordable-market purchases. At 3.5% down on the $541,287 floor, max purchase price is ~$560,900. |

| High-Cost / Ceiling CA, NY, HI, DC metro, CO, WA, etc. |

$1,249,125 | $1,599,375 | $1,933,200 | $2,402,625 | 150% of conforming limit. Same ceiling as 2026 Fannie/Freddie high-cost limit. Verify your county at hud.gov mortgage limits tool. |

| AK / HI / Guam / USVI Section 214 exception areas |

$1,873,687 | $2,399,050 | $2,899,800 | $3,603,925 | Adjusted up to 150% of ceiling for construction cost exceptions per National Housing Act §214. |

Key limit facts for 2026: The $541,287 floor — up 3.26% from $524,225 in 2025 — covers most first-time buyer purchases in the South, Midwest, and Mountain West. The national median home price is approximately $425,000 (NAR early 2026), well within the floor limit with a 3.5% down payment. Use the HUD Mortgage Limits search tool to find your exact county limit: hud.gov/program_offices/housing/sfh/lender/origination/mortgage_limits

FHA Loan Eligibility Checklist — 2026

Before applying, run through this checklist. Each row shows the FHA program minimum, the typical lender overlay (what most lenders actually require), and what you can do if you don’t currently meet the threshold.

| Requirement | FHA Program Minimum |

Typical Lender Overlay (2026) |

You Qualify? |

If You Don’t Qualify Yet |

|---|---|---|---|---|

| Credit Score | 500 (with 10% down) 580 (with 3.5% down) |

580–620 at most lenders Some accept 500–579 with 10% down + compensating factors |

☐ | Pay down revolving balances (target <30% utilization). Dispute errors on credit reports. Add authorized user status on a low-utilization card. New American Funding and Carrington are most flexible on 500–579. |

| Down Payment | 3.5% (580+ score) 10% (500–579 score) |

Same as FHA minimum Gift funds from family 100% allowed; DPA programs can cover all or part |

☐ | On $425K home, 3.5% = $14,875. Look into state DPA programs and local housing authority grants. Guild, loanDepot, and Fairway have strong DPA partnerships. Gift funds from family members are allowed — must be documented with gift letter. |

| Debt-to-Income Ratio (DTI) | 43% back-end (standard) 57% max (with AUS approval) |

43%–50% typical Higher allowed with 680+ score and reserves |

☐ | Pay off or down smaller debts first (car loans, credit cards). Adding a co-borrower’s income can offset high DTI. Manual underwriting allows higher DTI with strong compensating factors. |

| Employment & Income | 2 years employment history (same field, not necessarily same employer) |

Same — W-2, pay stubs, 2 yrs tax returns Self-employed: Schedule C + P&L + 2 yrs returns |

☐ | Gap in employment <6 months generally acceptable with explanation letter. Recent job change in same field OK. Gig/1099 income averaged over 24 months per updated HUD 2025 guidelines. |

| Primary Residence Only | Must be your primary residence (not investment or vacation) |

Same — must occupy within 60 days of closing | ☐ | FHA is primary residence only. For investment properties or second homes, look at conventional (3%+ down), DSCR loans, or Non-QM. Exception: FHA 203(k) rehabilitation loans allow purchase of 2–4 unit properties if you live in one unit. |

| No Active Federal Default | Clear CAIVRS check (no delinquent federal debt) |

Same — delinquent student loans, IRS debt, or prior FHA claims will block approval | ☐ | Must resolve any federal debt delinquencies before FHA will issue a case number. Enter a repayment plan for student loans or IRS installment agreement and document it. Lender will run CAIVRS check. |

| Bankruptcy Waiting Period | Chapter 7: 2 years from discharge Chapter 13: 1 year on-time plan payments (w/ trustee approval) |

Same as FHA minimum Credit rebuilt after discharge needed |

☐ | Extenuating circumstances (job loss, medical) can shorten Ch. 7 waiting period to 1 year with documented proof. Ch. 13 filers can get FHA after 1 year of on-time plan payments with court and trustee approval. |

| Foreclosure / Short Sale | 3 years from completion date | Same — 3-year minimum from recorded date Credit must be re-established |

☐ | Extenuating circumstances can shorten to 1 year. Document hardship (layoff, medical event) with supporting records. Some lenders offer non-QM “day 1” after foreclosure at higher rates. |

| Property Standards | Must meet FHA Minimum Property Requirements (MPRs) FHA appraisal required |

Same — FHA-approved appraiser must confirm safe, sound, secure | ☐ | If property fails MPR (roof, foundation, safety hazards), seller must repair before closing or use FHA 203(k) loan to finance purchase + repairs in one transaction. Condos must be on FHA-approved condo list. |

| Loan Amount | Must be at or below FHA county limit (see limits table above) |

Same — loan amount cannot exceed county FHA limit | ☐ | If purchase price exceeds local FHA limit, options are: (1) larger down payment to reduce loan amount below limit, (2) conventional financing ($832,750 conforming baseline), or (3) jumbo mortgage for high-cost areas. |

FHA Mortgage Insurance Premium (MIP) Schedule — 2026

All FHA loans require two types of mortgage insurance: an upfront premium (UFMIP) and an annual premium (paid monthly). These are non-negotiable FHA program requirements — not set by individual lenders.

| MIP Type | Rate | When Paid | Duration | Dollar Example ($300K loan) |

|---|---|---|---|---|

| Upfront MIP (UFMIP) | 1.75% | At closing (can be rolled into loan) | One-time | $300,000 × 1.75% = $5,250 (added to loan if rolled in; new loan = $305,250) |

| Annual MIP (monthly) 30-yr loan, >90% LTV (most buyers) |

0.55%/yr | Monthly (in mortgage payment) | Life of loan if <10% down |

$300,000 × 0.55% ÷ 12 = $137.50/mo. Cannot be removed without refinancing out of FHA (unlike conventional PMI which cancels at 20% equity). |

| Annual MIP (monthly) 30-yr loan, ≤90% LTV (10%+ down) |

0.50%/yr | Monthly | 11 years then cancels |

$300,000 × 0.50% ÷ 12 = $125/mo. Cancels after 11 years if 10%+ was put down at origination — important to note for buyers who can stretch to 10% down. |

| Annual MIP (monthly) 15-yr loan, >90% LTV |

0.40%/yr | Monthly | Life of loan | $300,000 × 0.40% ÷ 12 = $100/mo. 15-year FHA loans have lower MIP rates — significantly cheaper for buyers who can handle the higher payment. |

MIP vs. conventional PMI — the key difference: Conventional PMI cancels automatically when equity reaches 20% of the original home value. FHA MIP for loans with less than 10% down payment cannot be removed — it stays for the life of the loan. To eliminate FHA MIP, borrowers must refinance into a conventional loan. This is typically worth doing when: credit score has improved to 700+, the home has appreciated to 80% LTV or better, and current mortgage rates are favorable. For borrowers putting 10%+ down at FHA origination, MIP cancels after 11 years.

FHA loan limits: HUD Mortgagee Letter 2025-21 (effective January 1, 2026); confirmed by FHA.com, Scotsman Guide, The Truth About Mortgage, and NMP (December 2025). Conforming loan limit $832,750: FHFA press release November 26, 2025. FHA MIP rates: HUD ML 2023-05 (0.55% annual for most 30-yr loans); FHA Mortgage Source March 2026. NMLS numbers: Pennymac #35953 (pennymac.com), Rocket Mortgage #3030 (rocketmortgage.com), Freedom Mortgage #2767 (freedommortgage.com), loanDepot #174457 (loandepot.com), Guild Mortgage #3274 (guildmortgage.com), New American Funding #6606 (IHDA lender list), Carrington Mortgage Services #2600 (carringtonmortgage.com), Fairway Independent Mortgage #2289 (fairwayindependentmc.com) — all verified from official lender licensing disclosures March 2026. FHA volume rankings per Scotsman Guide 2024 and The Truth About Mortgage 2024 origination analysis. Rate ranges are market estimates as of March 2026 and vary by credit score, LTV, and daily market conditions. This page is for informational purposes only and is not an offer to lend.

Look for FHA Lenders with Experience Approving Lower Credit Scores

Shopping for an FHA loan is easier than a conventional loan. FHA mortgages are backed by the US government, so lenders can extend credit to you at better terms than you might expect. FHA only has a minimum credit score of 500 to get an FHA loan.

- Compare the Top FHA Mortgage Lenders for Free

- Find the Best Banks for FHA Mortgages

- Shop Top FHA lenders for the Best Rates Online

Remember that FHA loans are not exclusively for first-time homebuyers; repeat buyers and homeowners looking to refinance get cash out and make home improvements can also benefit from this loan option.

But if you have a credit score under 600, you should start shopping for your FHA mortgage rate by checking with several poor credit score mortgage lenders.

The reason is that an FHA approved lender can have what are called overlays. This simply means lenders have the discretion to require a credit score higher than the 500 minimum set by FHA.

Some FHA approved lenders may have a minimum of 600, 620, or 640. The lower your score, the more lenders you should check. You could find a very similar program with two lenders where one has a rate .5% lower than the other.

Why These FHA Lenders Stand Out

These lenders dominate FHA lending due to high origination volumes (33% of 2023’s 580,000 FHA loans came from the top 10) and borrower-centric features. Pennymac excels with low-credit approvals, while Rocket’s digital platform speeds up closings. New American Funding prioritizes underserved communities, and CrossCountry offers rapid approvals. Fairway and Guild emphasize customer service and flexibility, while LoanDepot and builder-affiliated lenders like DHI and Lennar provide substantial financial assistance. Cardinal Financial’s purchase-loan focus suits FHA buyers.

Remember to Lock in Your FHA Mortgage Rate Early

As we noted earlier, it appears that FHA loan rates will be on their way down this year. Mortgage rates have stayed abnormally low despite the Fed raising the Prime Rate several times in the past 18 months. Rates have edged up in the last few months, but overall FHA mortgage rates remain attractive and competitively priced.

- Current FHA mortgage rates

- 30 year FHA mortgage rates

- 15-Year FHA interest rates

It seems likely this trend will persist. If you plan to close a loan in the next few months, it is smart to lock the rate for as long as you can. Even paying to lock it beyond two months is not out of the question. According to CNBC, interest rates are only going to go up this year as the economy gets even better than it is now.

FHA loans are great products that provide you with a lower than market rate even with average credit. You do have to pay a higher cost for mortgage insurance, but this cost is somewhat offset with the low rate. This means you really should be watching FHA loan rates like a hawk if you plan to close soon.

This probably is not a market to let the rate float and hope for lower rates. Time is running out on the artificially low rate environment for all loans – FHA, conventional and others.

2026 FHA Mortgage Requirements

FHA loans are backed by the Federal Housing Administration. This signifies that every loan endorsed by the FHA enjoys the full backing of the U.S. government’s faith and credit. This assurance implies that in the event of a borrower defaulting on the FHA loan, the Federal Housing Administration assumes responsibility for repaying the lender.

Consequently, numerous FHA-mortgage lenders can extend favorable credit terms and down payment options to individuals who may not otherwise qualify for a mortgage. FHA loans can secure approval with a 580-credit score and a 3.5% down payment, featuring highly flexible debt-to-income ratios and income requirements. While FHA mortgages are among the easiest to secure approval for in the United States, the duration of the approval and closing process may span several months depending on individual circumstances.

Popular FHA Mortgage Programs

- FHA-cash out refinance (203B)

- FHA streamline refinance

- FHA rehab loan (203k)

- FHA 40 Year Loan

- FHA construction loan

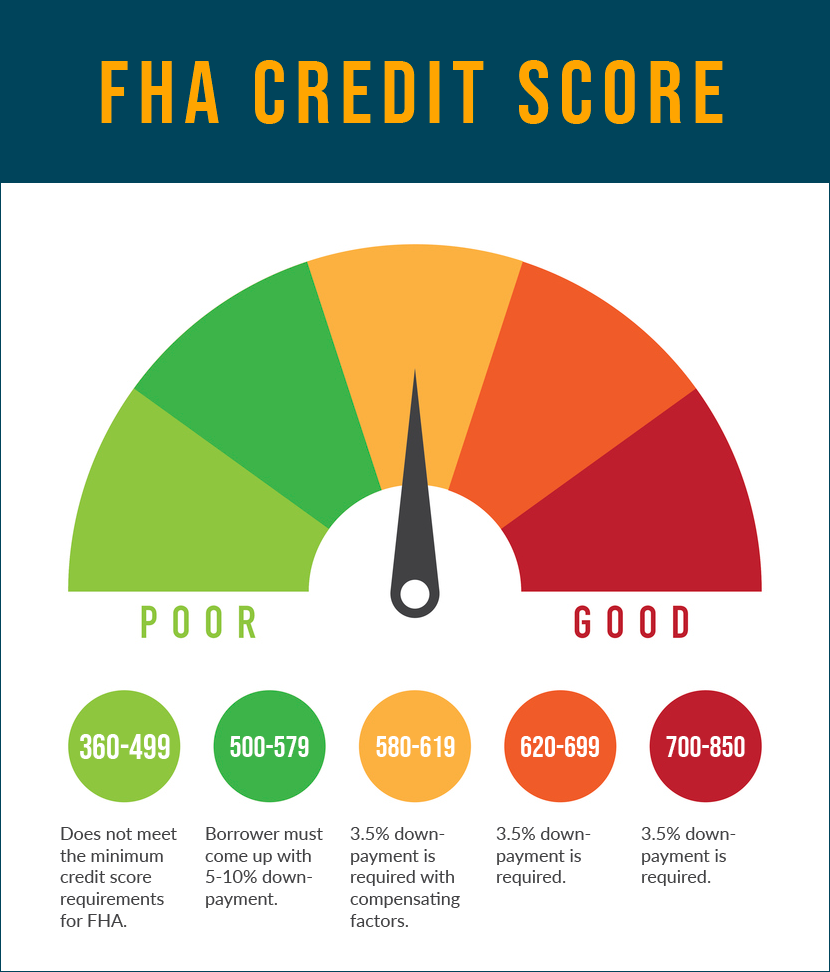

Credit Score Requirements for FHA Mortgages

FHA loans are a good deal for many of us with lower credit score. As of 2023, the Federal Housing Administration dropped the minimum credit score requirement for FHA loans to 500. In comparison, the minimum credit score for a conventional loan is 620 and 640 for USDA loans. While it is getting easier for people to get FHA loans, having a 500-credit score can make things difficult. Recent statistics show that you are better off with a higher credit score to qualify for an FHA loan. The minimum credit score rules will vary depending upon the mortgage company you are talking to. Learn more about the current FHA credit score requirements.

FHA Loan Credit Requirement Overview

What are the FHA mortgage requirements for a FHA insured mortgage this year? Direct endorsed FHA loan lenders now will approve more than 96% of people who have a FICO score of 580.

If your score is at least that high, you may qualify for a 3.5% down payment as well. This is one of the most lenient down payment requirements on the market.

Plus, underwriting standards are very forgiving in terms of credit score and debt to income ratios.

Let’s consider what it takes to qualify for FHA loans today.

If you have a 500-credit score, that is the minimum score that will be considered per FHA loan requirements. But know that you will have to put down 10% to get a loan at that FICO score.

Only 2% of FHA loans in the past year have gone to people with 500 to 549 credit scores.

Your best chance for a FHA loan approval with this low of a credit score is to show a clean payment history for the past 180 days and a good sized down payment.

There are many reasons you could have a lower credit score and still qualify for an FHA loan:

- You are using a lot of your available credit. This can lower your score by 50 points in some cases. But as you pay it off, your score will rise.

- You have a lot of credit accounts, or a lot of new credit accounts

- Your credit history is limited

- You had a foreclosure or bankruptcy in the past

FHA mortgage guidelines state that if you have made timely payments on your credit obligations in the recent past, you are a reduced risk. So, if you have a bankruptcy on your credit report from two years ago with sub 600 credit, this will not prevent you from getting an FHA loan.

On the other hand, if your credit report shows you have enough income to support your bills but have a lot of late payments, you are less likely to be approved, even if your score is higher. The best FHA loan lenders care the most about a steady payment history on your obligations in the past 12 to 24 months. This indicates a degree of financial stability that reduces lender exposure.

Where Is the Best Place to Get an FHA Loan?

The best place to get an FHA loan depends on your financial needs and preferences. Many banks, credit unions, and online lenders offer FHA loans. Well-known lenders like Rocket Mortgage, FHA.com, and Wells Fargo specialize in FHA financing. It’s best to compare rates, fees, and customer reviews before choosing a lender. Working with an FHA-approved lender ensures you receive competitive rates and the best guidance for your home-buying process.

How Do I Get an FHA Pre-Approved Mortgage?

To get FHA pre-approved, start by choosing an FHA-approved lender and submitting a pre-approval application. The lender will review your credit score, income, debt-to-income ratio (DTI), and employment history. You’ll also need to provide financial documents like tax returns and bank statements. If approved, you’ll receive a pre-approval letter, which strengthens your offer when shopping for a home. This process typically takes a few days to a few weeks.

What Documents Do I Need for the FHA Loan Checklist?

When applying for an FHA loan, you’ll need:

- Proof of income (pay stubs, W-2s, or tax returns)

- Bank statements (last two months)

- Employment verification

- Credit report & score check

- Debt and asset information

- Property details (if available)

Providing accurate documents ensures faster loan processing and approval. Your lender may request additional documents, depending on your financial situation.

Who Are the Best FHA Lenders for First-Time Home Buyers?

The RefiGuide can help you shop and find the best FHA lenders for first-time home buyers online. The top FHA lenders include Loan Depot, Rocket Mortgage, Chase, and New American Funding. These approved FHA lenders offer low down payment options, flexible credit requirements, and strong customer support. FHA-approved lenders specializing in first-time buyers often provide educational resources and loan programs to help navigate the home-buying process. Comparing FHA mortgage rates and loan terms is essential to finding the best lender for your needs.

What Is Included in FHA Loan Closing Costs?

You can expect to pay for the following closing costs on FHA mortgages. A percentage of these closing costs can be rolled into or financed into the FHA loan:

- Loan origination fee: Percentage of the amount of the loan that the lender charges you

- Discount points to lower rate: 1-point equals 1 percent of the loan amount

- Appraisal fee: What you have to pay to have the home appraised

- Credit report: Charge to pull your credit report

- Tax service: Lender hires a company to ensure there are no liens or taxes owed

- Title insurance: Covers any legal damages if the seller cannot transfer the title legally. This protects the mortgage lender and borrower.

- Attorney fees: What the attorney charges for overseeing the transaction at the title company

- Document fees: FHA lender will charge you to have the many documents ready for closing

- Property taxes: You are charged the remaining yearly property taxes on the home

- Home inspection: Covers cost of having the home inspected

- Survey: The fee to get accurate boundary and property measurements by the surveyor

- FHA Mortgage Insurance Premium: Borrowers that get an FHA loan will be required to pay mortgage insurance every month.

The bottom line is that in some cases, you can reduce your out of pocket expenses when you buy the home by having your closing costs financed or otherwise paid for. Check with your approved FHA lender to see what options you when considering buying a home with FHA financing.

Remember to Account for Mortgage Insurance

FHA loans are great for many situations, but you have to pay for expensive mortgage insurance to get that low interest rate. There are two types of mortgage insurance on FHA mortgages. The first one is an upfront premium of 1.75% of the loan amount. That is $1,750 for a $100,000 loan. That can be rolled into the mortgage.

The other type of FHA mortgage insurance has the annual premium that is paid each month. The amount varies on the loan length and the loan to value or ‘LTV’. For a 30-year FHA loan with a down payment of less than 5%, your annual insurance premium with be .85% of the loan amount. The reality is that the FHA mortgage insurance premium is the reason people can get an FHA loan with only a 3.5% down-payment in 2023.

The FHA Lender Must Be Approved to Issue FHA Loans

Know that FHA does not lend money; it merely insures the loan issued by a lender. So borrowers need to get an FHA loan through a lender approved by the agency. Not all FHA loan lenders offer the same rates. Some have investors who want more security and charge a higher rate, while others are willing to offer a lower rate.

How to Assume an FHA Mortgage

Are FHA Loans Assumable? FHA mortgage loans offer the advantage of being assumable, a feature that can prove beneficial for both buyers and sellers. In essence, an assumable mortgage permits a homebuyer to take over the existing FHA loan along with its terms when purchasing a property.

For prospective buyers, assuming an FHA mortgage holds several advantages, particularly if the current FHA mortgage rate is lower than the prevailing market rates. This can result in substantial savings over the duration of the FHA home loan. Furthermore, the process of assuming an FHA loan often involves less rigorous credit requirements compared to securing a new mortgage.

Sellers can also reap the rewards of the assumable feature. It can enhance the marketability of their property, particularly when interest rates are on the rise. The ability to offer a potential buyer an assumable FHA loan can make the property stand out in a competitive real estate market.

Are All FHA Loans Assumable?

However, it’s crucial to note that not all FHA home loans are assumable. For FHA loans initiated after December 1, 1986, the assumption necessitates approval from the lending institution, and specific criteria must be met. The prospective buyer must also qualify for the assumption by demonstrating their creditworthiness and their capacity to meet the obligations of the FHA loan. It’s essential for all parties involved to have a comprehensive understanding of the terms and payment responsibilities associated with assuming an FHA mortgage before committing to this option. It’s important to be aware that if a homebuyer takes over an FHA loan, they will also be obliged to make monthly payments for FHA mortgage insurance premiums.

Does the Federal Housing Agency Make Loans?

The FHA itself does not provide mortgage financing. Instead, the loan is issued by a bank or another financial institution that is FHA-approved. The FHA guarantees the loan, which reduces the risk for the bank and makes it easier for borrowers to obtain approval. This is why such loans are often referred to as FHA-insured loans.

Borrowers who qualify for an FHA loan must purchase mortgage insurance, with the premium payments directed to the FHA. Read more about FHA and the Consumer Financial Protection Bureau.

How to Qualify for a FHA Loan with No Mortgage History

Do you want to buy a home and have limited credit history, no credit history, or no mortgage history? You are not alone. Many first-time home buyers face significant challenges in buying their first house. Specifically, many lack a long credit history. This makes it more difficult for lenders to determine your risk profile and decide to give you a loan.

Most first-time home buyers have never had a mortgage or have not had one in years. They also may own their car in cash and may use their debit card rather than credit cards. These traits make many new house buyers off the grid when it comes to credit and may make getting a mortgage more challenging.

If you think there is no hope, you are wrong: The FHA loan is available to people buying a home for the first time with little credit or no credit. And, FHA backed mortgages can be had from most mortgage lenders in the US.

FHA Loans and Non-Traditional Credit

First-time home buyers typically possess lower credit scores compared to homeowners, primarily because they have had less time to establish a credit history. Payment history plays a pivotal role in determining one’s FICO score.

However, it’s important to note that the solution is not necessarily obtaining a credit card or taking out a car loan, as these actions can temporarily negatively impact your credit score.

Credit score algorithms tend to view acquiring new credit lines as a drawback. Moreover, the impact on your credit score remains limited until the payment history on the account spans at least 12 months.

A more advisable approach, as recommended by many experts, is to explore mortgage loans tailored for individuals with limited credit histories, such as the FHA loan. Sponsored by the Federal Housing Administration, this program explicitly states on its website that a lack of credit history or limited credit usage should not serve as grounds for rejecting a loan application.

Instead of turning away applicants lacking credit history or prior mortgage experience, FHA loan guidelines necessitate lenders to scrutinize every facet of the loan application.

FHA has the flexibility to consider your rental history as a crucial aspect. If you can demonstrate consistent, on-time rent payments over the last one or two years, provided they are in line with potential mortgage payments, this can serve as a basis for approving a mortgage.

Furthermore, FHA allows lenders to require minimal down payments, with the current minimum being just 3.5%, a highly reasonable option for first-time home buyers. Often, these buyers face challenges in amassing substantial down payments, especially when they lack equity in an existing home.

Additionally, issues related to bad credit loans for first-time home buyers are not insurmountable with FHA, as they permit lenders to accept credit scores as low as 580 with a 3.5% down payment. The program also accommodates higher debt-to-income ratios.

Approval Up to the FHA Mortgage Lender?

FHA home loans are underwritten by private lenders that have been approved to do FHA loan programs. All lenders must follow FHA guidelines, but these rules are not absolute when it comes to credit score. Some lenders may work with a borrower with a 580-credit score, while others only work with borrowers with a higher score. If you have a credit score lower on the scale, it is wise to check with several of the best FHA lenders. If you cannot qualify with one lender, you might be able to with another.

Generally, getting an FHA loan approved with a 500 score will be arduous. You will need to have solid income, 10% down payment, and probably some cash reserves. People with a 580 or higher score only need 3.5% down usually, and no cash reserves are needed.

In addition to an acceptable credit score, you must demonstrate enough income to pay the loan and a reasonable amount of debt. Generally, you should have a front-end ratio of 31% and a back-end ratio of 43% to qualify for an FHA loan program. This means your mortgage debt compared to your gross monthly income should not be a ratio of more than 31%, and your total debt compared to your gross monthly income should not be more than 43%.

However, some of the best FHA loan lenders might allow those ratios to go higher if you have enough income and reserves. Others with higher credit scores may also be able to be approved with higher debt to income ratios.

According to current FHA statistics, there is a big market in the country for loans for people with a limited credit history – up to five million households across the country. So, it is important to not let your lack of credit history discourage you from applying for a mortgage.

How to Qualify for FHA Loans After a Chapter 7 Bankruptcy

Many individuals hold the mistaken belief that obtaining a mortgage after a bankruptcy is a prolonged process spanning seven to ten years. This misconception is far from the truth. In the aftermath of the mortgage crisis, a substantial number of people found themselves declaring bankruptcy. For the housing market to thrive, it’s crucial that the top FHA lenders do approve loans for individuals with recent bankruptcies.

The established standard for securing approval for an FHA loan after a Chapter 7 bankruptcy is a two-year waiting period, and it shortens to just 12 months for Chapter 13. The primary focus here is demonstrating to both FHA and its lending institutions that you’ve maintained a solid payment history over the past 12 to 24 months.

In such cases, a prior bankruptcy need not be an impediment. Furthermore, FHA loans remain a viable option even after a foreclosure. Significantly more individuals faced foreclosures following the mortgage crisis than those who declared bankruptcy. Typically, the waiting period for FHA loans is three years, although some mortgage brokers may have more flexible criteria. It’s advisable to inquire within the lending community to explore your options.

What is the Energy Efficient FHA Mortgage?

The FHA Energy Efficient Mortgage (EEM) is a special FHA loan financing program designed to empower homeowners to make energy-efficient improvements to their properties. This unique FHA loan program allows borrowers to include the cost of energy-efficient upgrades into their FHA insured mortgage.

By doing so, homeowners can finance projects such as solar panels, insulation, or energy-efficient HVAC systems, facilitating the creation of an environmentally friendly and energy-efficient houses. The primary advantage of the FHA energy efficient mortgage is that it enables borrowers to make these improvements with minimal upfront costs.

The cost of the energy-efficient upgrades is rolled into the mortgage, and the increased monthly payments are offset by the anticipated energy savings, making it a financially sensible choice. This innovative FHA loan program aligns with the growing emphasis on sustainable living and allows homeowners to contribute to both a greener environment and long-term cost savings. FHA EEM serves as a practical and accessible avenue for those seeking to enhance their homes while embracing energy efficiency.

What to Expect with FHA Mortgage Programs in 2026

The FHA loan limits were raised by the US Congress for the coming year and will continue to be a popular choice for first time home buyers and people with average credit scores. FHA loan limits should continue to rise with home values and inflation continuing to soar.

- Secure a FHA Mortgage Preapproval

- Check FHA Mortgage Rates Today

- Shop for the Best FHA Loans

- Apply with Trusted FHA Mortgage Lenders

All indications point to FHA mortgage rates falling in 2026 and with the elections coming up you can expect the Federal Reserve will play an important role in affordability for new home buyers and homeowners looking to lower their monthly payments with the best FHA loan rates we have seen in a few years.

Last reviewed: March 23, 2026 by Bryan Dornan, Mortgage Lending Expert and Founder of RefiGuide.org.

About Bryan Dornan

Bryan Dornan is a financial journalist and mortgage industry veteran with nearly 30 years of experience as a lender, loan officer, mortgage broker, and chief marketing officer. He currently serves as Chief Editor of RefiGuide.org, where he has built one of the most trusted mortgage education platforms in the United States. Bryan has founded multiple mortgage and digital marketing companies throughout his career and remains focused on helping homeowners leverage home equity wisely while making affordable homeownership accessible to everyday Americans. He is a licensed California Real Estate Broker DRE: #01203791. and writes for RealtyTimes, Patch, Buzzfeed, Medium and other national publications. Find him on Twitter, Muckrack, and Linkedin

More articles by Bryan Dornan