VA home loans are attractive and not out of reach if you meet the VA loan requirements and qualifications. Are you active or retired military? You may be able to qualify for a Veteran’s Administration financing, also known as the VA loan. Our team will educate you on the current VA home loan guidelines. These Veteran mortgages are unique and powerful finance options for select American borrowers. The RefiGuide breaks down the VA loan requirements for 2026.

Who Qualifies for a VA Home Loan in 2026?

Eligible applicants include active-duty service members, Veterans with an honorable discharge, National Guard or Reserve members with at least six years of service, and certain surviving spouses—who must also obtain a Certificate of Eligibility and meet lender credit, income, and occupancy criteria

The VA mortgage loan is highly regarded as the most sought after home financing product in the United States. The VA home loan requirements make buying a house easy if you meet the VA eligibility that we will outline below. Find Low Credit VA Home Loans, Low Rates with No Down Payment Required!

VA loans typically have no down payment requirements and offer lower interest rates to buy a home compared to traditional mortgage products. They are also more flexible, allowing for higher debt-to-income ratios and lower credit scores, and they do not require mortgage insurance or PMI.

For borrowers who are or were in the US military, VA home loans are one of the best options for people serving in the U.S. Armed Forces to buy a house. The U.S. Government Expanded the VA Loan Program to Help More Military Families in the Army, Air Force, Navy, Marines, Coast Guards and Reserves Finance New Homes or Refinance Existing Mortgages. There is no down payment to buy a home required with any VA loans.

If you want to buy a home and are a military veteran or active duty, keep reading to learn more about current VA home loan guidelines for 2026.

VA home financing offers significant benefits to military borrower that served their country. People who qualify for a VA home loan do not have to deal with as much hassle as far as getting approved for a VA loan option, and the veteran home loan rates are usually excellent as well. The RefiGuide can help you get educated on VA loan requirements while getting you a preapproved for a mortgage.

How VA Home Loan Rates Work

Like conventional mortgage rates, VA mortgage rates fluctuate with the market. They also depend on the repayment term you choose. VA approved lenders typically offer lower interest VA purchase rates for 15-year mortgages than for 30-year loans due to the shorter repayment period and reduced risk.

The VA loan rate you qualify for can be either fixed or adjustable. With a fixed interest rate, you’re guaranteed the same rate for the duration of your VA backed loan. A variable interest rate mortgage will have a fixed rate for an initial period, after which it will adjust periodically based on market conditions.

VA mortgage rates, like all consumer borrowing rates, have risen in recent years following a series of interest rate hikes by the Federal Reserve the last few years. While the Federal Reserve does not directly set mortgage interest rates, its policies significantly influence borrowing costs.

Overview of VA Home Loan Guidelines

Here are some of the key things to know about VA home financing in 2026:

- No down payment needed: For most Americans, no down payment home loans are a thing of the past. The closest most people can get is a 3.5% down-payment issued via FHA loan guidelines. But if you can qualify for a VA loan, it usually can be with no money down. Qualified VA borrowers love the $0 down home loans. All you need to pay is closing costs and the VA funding fee. Borrowers love the no down payment requirement with the VA backed zero down purchase loans.

- No mortgage insurance: If you qualify for the VA loan benefit, you do not have to pay for mortgage insurance or PMI. This is usually required for people who have less than 20% stake in the property. PMI will typically add $100 or more to your monthly payment.

- Flexible lending requirements: Many other lenders have higher credit standards than a decade ago. But the VA mortgage is a military benefit, so the standards are quite flexible. As long as you have a credit score of 620 or higher, you should be able to qualify for the VA home loan benefit.

- Low interest VA loan rates: VA mortgages are usually lower than market rates, so you should be able to have one of the lowest possible monthly payments.

- No pre-payment penalties: If you want to pay off the purchase loans early or refinance, you will not be penalized.

VA Home Loan Requirements

You are eligible for VA loan terms if you meet one of the following criteria:

- Completed at least 90 days of active duty service.

- Served at least six years in the Reserves or National Guard.

- Completed at least 181 days of active duty service during peacetime.

- Accumulated 90 days of cumulative service under Title 10 or Title 32, with at least 30 consecutive days for Title 32 service.

You can initiate a VA loan application through a bank, mortgage company, or credit union that provides such services. The VA home loan application process resembles that of other mortgage types: you provide employment, income, and financial details, and the lender evaluates your eligibility.

How to Get a Pre-Approval for a VA Home Loan

An essential requirement is obtaining a VA certificate of eligibility, a document issued by the Department of Veterans Affairs verifying your fulfillment of the service prerequisites for a VA loan. You can acquire this document directly from the VA or request a VA mortgage lender to obtain it on your behalf.

Once you have shown a lender your income, tax and payroll documentation, he or she can give you a pre-approval letter. This letter is usually needed when you are going to look at homes and need the lender to state that you are pre-approved for purchase loans that are VA guaranteed. The owner of the property wants to see that you have the ability to get a home loan.

The VA pre-approval letter will usually say that you have been pre-approved for a VA loan up to a certain amount. You will still need to fully qualify for the VA loan eligibility, but the pre-approval letter is a critical step.

Those are the most important features of buying a home guaranteed by the VA today. The VA loan requirements have not changed much of the last few years. Now let’s examine what you need to qualify.

What Are VA Home Loan Amounts in 2026?

One of the most important updates veterans need to know: the VA no longer imposes a loan limit for borrowers with full entitlement. The Blue Water Navy Vietnam Veterans Act, effective January 1, 2020, eliminated VA loan caps for eligible veterans and service members who have their complete entitlement available. This means a qualified borrower with full entitlement can purchase a home at any price — $500,000, $1 million, or more — with zero down payment, as long as they meet lender income, credit, and DTI requirements and the property appraises at the purchase price.

Loan limits only apply to veterans with partial entitlement — meaning they have an active VA loan on another property, have previously defaulted on a VA loan, or sold a home without fully restoring their entitlement. For these borrowers, the 2026 baseline conforming loan limit of $832,750 (set by FHFA on November 25, 2025) determines their zero-down buying ceiling. See the complete loan limits table in the section below.

2026 VA Loan Limits by County

Since January 1, 2020, the VA does not impose loan limits for veterans with full entitlement — you can purchase a home of any value with zero down as long as you financially qualify and the property appraises at the purchase price. This applies even in markets where homes cost $1.5 million or more. Loan limits only matter if you have partial entitlement (an active VA loan on another property, or unrestored entitlement from a prior VA loan). The information below applies to the partial-entitlement scenario.

For 2026, FHFA announced updated conforming loan limits on November 25, 2025, effective January 1, 2026. These limits reflect a 3.26% increase in average U.S. home prices and directly determine the VA’s guaranteed amount for partial-entitlement borrowers.

2026 Baseline and Ceiling Limits (Most Borrowers)

The loan limits table is further down. I can see the page content and know the VA loan limits data from our session. The “2026 Baseline and Ceiling Limits” table covers loan limits by property type. That’s a straightforward 4-column table — already the right count for mobile. Here it is, tightened and clean:

VA Loan Limits 2026 — Baseline and Ceiling Limits (Most Borrowers)

| Property Type | Units | Baseline Limit (Most U.S. Counties) | High-Cost Ceiling (e.g., CA, HI, NY, DC) |

|---|---|---|---|

| Single-Family Home | 1 unit | $806,500 | $1,209,750 |

| Duplex | 2 units | $1,032,650 | $1,548,975 |

| Triplex | 3 units | $1,248,150 | $1,872,225 |

| Fourplex | 4 units | $1,551,250 | $2,326,875 |

Loan limits per FHFA 2026 conforming loan limit announcement (effective January 1, 2026). VA does not set its own loan limits — VA loan limits match FHFA conforming loan limits county by county. Borrowers with full VA entitlement (no prior VA loan in use) have no effective loan limit and can borrow above these figures without a down payment, subject to lender and VA approval. Borrowers with partial entitlement (active prior VA loan) are subject to the county loan limit. High-cost limit applies to designated high-cost counties — verify your county limit at fhfa.gov or with your VA-approved lender. Updated March 2026.

Key High-Cost Counties — 2026 VA Loan Limits (1-Unit / Single-Family)

| County | State | 1-Unit VA Loan Limit | Why It’s High-Cost |

|---|---|---|---|

| San Jose-Sunnyvale-Santa Clara | CA | $1,209,750 | Silicon Valley — national ceiling · among the most expensive housing markets in the U.S. |

| San Francisco-Oakland-Berkeley | CA | $1,209,750 | Bay Area tech hub · at the national high-cost ceiling |

| Los Angeles-Long Beach-Anaheim | CA | $1,209,750 | Largest CA metro · SoCal demand drives limit to national ceiling |

| San Diego-Chula Vista-Carlsbad | CA | $1,209,750 | Major military hub (MCAS Miramar, NAS North Island, Camp Pendleton) · at national ceiling |

| Honolulu | HI | $1,209,750 | Island geography restricts supply · at national high-cost ceiling |

| Maui County | HI | $1,209,750 | Limited land supply · resort market premium |

| Washington DC (DC proper) | DC | $1,209,750 | Federal government employment hub · at national ceiling |

| Arlington County / Alexandria | VA | $1,209,750 | DC metro spillover · Pentagon corridor · at national ceiling |

| Fairfax County | VA | $1,209,750 | DC suburb · highest median income county in the U.S. |

| Montgomery County | MD | $1,209,750 | DC suburb · NIH / federal agency hub |

| Nassau-Suffolk (Long Island) | NY | $1,209,750 | NYC metro · commuter premium · at national ceiling |

| New York City (5 boroughs) | NY | $1,209,750 | Highest density market · at national ceiling |

| Westchester County | NY | $1,209,750 | NYC suburb · among highest home prices in the Northeast |

| Nantucket County | MA | $1,209,750 | Island resort market · extreme supply constraint |

| Dukes County (Martha’s Vineyard) | MA | $1,209,750 | Island resort market · extreme supply constraint |

| Boulder County | CO | $1,034,400 | University + tech market · above baseline, below ceiling |

| Eagle County (Vail) | CO | $1,209,750 | Mountain resort market · at national ceiling |

| Pitkin County (Aspen) | CO | $1,209,750 | Luxury ski resort market · at national ceiling |

| Seattle-Tacoma-Bellevue | WA | $977,500 | Tech sector (Amazon, Microsoft) · above baseline |

| King County | WA | $977,500 | Seattle core county · major military installations nearby (JBLM) |

VA loan limits match FHFA 2026 conforming loan limits by county (effective January 1, 2026). The national baseline is $806,500 for a 1-unit property. The national high-cost ceiling is $1,209,750 — 150% of the baseline. Borrowers with full VA entitlement have no hard loan limit and can borrow above these figures without a down payment, subject to lender approval. Partial-entitlement borrowers are subject to the county limit. Verify your specific county at fhfa.gov or with your VA-approved lender. Updated March 2026.

How to Calculate Your Zero-Down Limit (Partial Entitlement)

If you have partial entitlement, use this four-step formula your lender will apply:

- Find your county’s 2026 one-unit conforming limit (from the table above or FHFA.gov)

- Multiply by 25% = maximum VA guaranty for your county

- Subtract entitlement already used (shown on your Certificate of Eligibility) = remaining bonus entitlement

- Multiply remaining entitlement by 4 = your approximate zero-down purchase ceiling

Example: Your county limit is $832,750. You have $50,000 of entitlement tied to an existing VA loan. Maximum guaranty: $832,750 × 25% = $208,187. Remaining: $208,187 − $50,000 = $158,187. Zero-down ceiling: $158,187 × 4 = ~$632,748. Anything above that requires a 25% down payment on the excess amount.

If you want to buy above your zero-down ceiling, a down payment is not necessarily prohibitive — you only put down 25% on the amount exceeding your remaining entitlement, not 25% of the total purchase price. A VA lender can run this calculation in minutes once they pull your COE.

What Are VA Loan Rates Today?

VA purchase and refinance rates track the broader mortgage market, moving with the 10-year Treasury yield and Federal Reserve policy. The Fed held its benchmark rate unchanged at its March 17–18, 2026 meeting — the second consecutive hold — citing inflation pressures from oil prices tied to the Iran conflict. The MBA Refinance Index climbed 69% year-over-year as of March 18, 2026, reflecting strong borrower activity as rates remain well below the 2023 peak of 7.79%.

The VA loan’s most powerful rate advantage isn’t just the headline rate — it’s the elimination of monthly mortgage insurance. On a $400,000 purchase with 5% down, a conventional borrower pays $150–$250/month in PMI until reaching 20% equity. A VA borrower pays nothing monthly, even with zero down. Over five years, that adds up to $9,000–$15,000 in avoided PMI costs — far exceeding the one-time funding fee in most scenarios.

Please note that VA mortgage rates are subject to daily market fluctuations. Consult directly with VA-approved lenders or financial advisors to obtain your personalized rate based on your specific credit profile, loan amount, and entitlement status.

VA mortgage rates remain among the most competitive in the market, typically running 0.25% to 0.50% below conventional 30-year fixed rates for the same borrower profile. As of the week of March 19, 2026, the Freddie Mac PMMS benchmark for 30-year fixed mortgages is 6.22%. VA purchase rates for well-qualified borrowers (700+ FICO, full entitlement) are running approximately:

| Loan Product | Approx. Rate (March 2026) | vs. Conventional | Notes |

|---|---|---|---|

| 30-year fixed VA purchase | 5.875% – 6.25% | ~0.25–0.50% lower | No PMI; zero down available; funding fee applies |

| 15-year fixed VA purchase | 5.50% – 5.875% | ~0.25–0.50% lower | Higher payment; faster equity build; lower total interest |

| VA IRRRL (streamline refi) | 5.875% – 6.00% | Best refi rate available | 0.5% funding fee; no appraisal required in most cases |

| VA cash-out refinance | 6.00% – 6.40% | Below conventional cash-out | Up to 90%–100% LTV; 2.15% or 3.30% funding fee |

| VA jumbo (above $832,750) | 6.25% – 6.75% | Varies by lender | Full-entitlement borrowers: zero down; lender overlays apply |

Rate ranges reflect well-qualified borrowers. Navy Federal Credit Union advertises VA rates as low as 7.00% APR for certain products; Veterans United posts rates from 6.80%–7.40% APR depending on product and points. Rates change daily — always get a same-day Loan Estimate. Source: Freddie Mac PMMS March 19, 2026 (30-yr benchmark 6.22%); Navy Federal rate sheet March 2026; VA loan network lender data March 2026.

VA Funding Fee 2026: Complete Rate Table

The VA funding fee is a one-time charge paid at closing on most VA-backed loans. It keeps the VA loan program self-sustaining without requiring taxpayer subsidies — which is what allows the VA to offer zero-down financing and no monthly mortgage insurance to future generations of veterans. The fee can be paid upfront at closing or rolled into the loan balance (the most common choice, adding it to your financed amount).

Current VA funding fee rates have been in effect since April 7, 2023, and are locked through November 14, 2031 per the Veterans Benefits Administration. Rates set by the U.S. Department of Veterans Affairs and confirmed by VA.gov.

Purchase and Construction Loans

| Down Payment | First Use of VA Benefit | Subsequent Use | Dollar Example on $350,000 Loan |

|---|---|---|---|

| 0% – 4.99% (No down payment) |

2.15% | 3.30% | $7,525 first use $11,550 subsequent |

| 5% – 9.99% | 1.50% | 1.50% | $5,250 (both) |

| 10% or more | 1.25% | 1.25% | $4,375 (both) — lowest available |

Refinance Loans

| Refinance Type | First Use | Subsequent Use | Notes |

|---|---|---|---|

| VA IRRRL (Streamline Refinance) | 0.50% | 0.50% | Lowest fee available; same rate regardless of prior VA loan use |

| Cash-Out Refinance | 2.15% | 3.30% | Down payment cannot reduce this fee; applies to full loan amount |

| Loan Assumption | 0.50% (all borrowers) | Paid by the borrower assuming the loan | |

VA Funding Fee Exemptions — Who Pays $0

The following borrowers are completely exempt from the VA funding fee and pay nothing:

| Exempt Borrower Category | Requirement | Estimated Savings on $350K Loan |

|---|---|---|

| Service-connected disability | Receiving VA disability compensation at any level (10%+), OR eligible for compensation but receiving military retirement pay instead | $7,525 – $11,550 |

| Purple Heart recipients | Active-duty service members who have received the Purple Heart and can provide evidence before closing | $7,525 – $11,550 |

| Surviving spouses (DIC) | Spouses of veterans who died in service or from a service-connected disability, receiving Dependency and Indemnity Compensation | $7,525 – $11,550 |

| Pre-discharge disability rating | Active-duty service members with a proposed or memorandum disability rating before closing | $7,525 – $11,550 |

Important: Approximately 6 million of the 18 million U.S. veterans receive VA disability compensation and qualify for a full exemption. If you have any service-connected disability rating, confirm your exempt status with your lender before closing — the fee cannot easily be removed after closing. Exemption status is verified through your Certificate of Eligibility (COE).

Strategic tip — the 5% threshold: If you are a subsequent-use borrower (using your VA benefit a second time or more) with no down payment, your fee jumps to 3.30%. Contributing just 5% drops that fee to 1.50%, saving $6,300 on a $350,000 loan. For subsequent-use borrowers with some savings, crossing the 5% threshold is often the highest-return financial move available at closing. Source: VA.gov funding fee and closing costs | NerdWallet VA funding fee analysis, 2026.

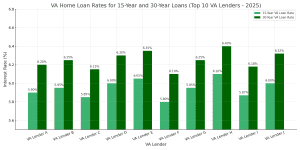

Top VA Mortgage Lenders in the US in 2026

VA home loans, backed by the Department of Veterans Affairs, offer veterans and active-duty members zero-down-payment mortgages with competitive rates and no private mortgage insurance. Below are the top 11 U.S. lenders offering VA loans in 2026, with estimated rates, APRs, and lending niches. Rates assume a 30-year fixed VA loan, 700+ credit score, and 100% loan-to-value (LTV), but vary by borrower. Closing costs range from 1–3% ($2,000–$6,000 on a $200,000 loan).

-

Veterans United (Columbia, MO): 6.80%–7.40% APR. Largest VA lender, free credit counseling, 14.69% market share.

-

United Wholesale Mortgage (Pontiac, MI): 6.85%–7.45% APR. Broker-only, 8.79% market share, 2% down grant for low-income borrowers.

-

LoanDepot (Lake Forest, CA): 6.90%–7.50% APR. Online process, 22-day closings, NAF Cash for all-cash offers.

-

Freedom Mortgage (Mount Laurel, NJ): 6.85%–7.45% APR. First-time buyer focus, Eagle Eye rate alerts, 4.36% market share.

-

Navy Federal Credit Union (Vienna, VA): 6.75%–7.35% APR. Military-focused, Military Choice loan, below-average rates.

-

DHI Mortgage (Austin, TX): 6.90%–7.50% APR. Homebuilder-affiliated, 2.85% market share, fast closings.

-

Village Capital (San Francisco, CA): 6.85%–7.45% APR. VA/FHA refinancing specialist, 2.62% market share.

-

Guild Mortgage (San Diego, CA): 6.80%–7.40% APR. 540+ credit for VA, non-traditional credit accepted.

-

New American Funding (Tustin, CA): 6.80%–7.40% APR. 500+ credit for VA, underserved borrower focus, 14-day closings.

-

PenFed Credit Union (McLean, VA): 6.75%–7.35% APR. No military affiliation needed, low APRs, $5 membership.

-

Flagstar Bank (Troy, MI): 6.80%–7.40% APR. 580+ credit, Military Choice loan, first-responder discounts.

Key Features for VA Loans

All lenders offer VA purchase and refinance loans, requiring a Certificate of Eligibility and 580–620+ credit. Niches include low-credit options (Guild, New American), military-focused lending (Navy Federal, Veterans United), and fast closings (LoanDepot). APRs range from 6.75%–7.50%, with VA funding fees (1.25–3.3%). Compare VA loan quotes to maximize savings.

Military Service Requirements for VA Loans

You have to be eligible for a VA loan option to get one. Active military and veterans must mean certain qualification standards regarding their service. The current standards to qualify from a service perspective are:

- Serve at least 90 consecutive days active during wartime

- Serve at least 181 consecutive days during peacetime

- Serve at least 6 years for the National Guard or Reserves

- Be the surviving military spouse for those who died in the line of duty or with a service-related, major disability

At least one of the aforementioned service requirements must be satisfied. In the event that they are not met, an alternative avenue to eligibility is to be the spouse of a military member who either lost their life in the line of duty or due to a service-related disability.

Typically, remarriage is not allowed. If you meet some or all of these requirements, you qualify for a VA home loan from a service perspective. You will still need to qualify financially, however.

Note: A co-borrower on the VA loan eligibility must also be a veteran or the spouse of the primary borrower who meets the criteria. Don’t forget that VA loan requirements can change so verify you and your co-borrower still meet the criteria.

Credit for VA Home Loan Qualification

VA loans are very flexible in terms of qualifying, but you will still need to have acceptable credit to get a VA-house loan.

VA loans are very flexible in terms of qualifying, but you will still need to have acceptable credit to get a VA-house loan.

Here are some of the common things you will need to answer with your lender:

- Credit score: As long as it is 620 or higher, you should be able to qualify with most VA mortgage companies.

- If you are lower than that, you may have problems. Ask the lender to check with all three credit bureaus and try to get a score at or above 620. However some VA approved lenders will offer VA loans for bad credit as long as the borrower meets the other VA guidelines.

- Collections or judgments: If you have past due accounts or accounts that have gone into collection, you may have problems getting a VA loan until those are resolved.

- Foreclosures or bankruptcies: If you have a bankruptcy or foreclosure, you will usually need to wait at least a year before being approved for VA loans to buy a home.

- Current income: Is your income stable and can you afford the monthly payment? Even though most veterans can get the VA home loan benefit, the lender must ensure that you have the ability to pay the loan.

What Are VA Home Loan Amounts?

How much home you can buy with a VA loan depends upon your income and debts, but most lenders currently cap VA loans at $417,000. Higher than that and VA will not pay back the lender in case you default. The VA loan limit is higher than FHA and conventional mortgages in most cases.

What Are Closing Costs on VA Loans?

All mortgages have closing costs. VA purchase loans still have lending fees and closing costs. These VA closing costs can range from 1 to 5% of your loan amount. However, the seller is allowed to cover up to 4% of the home’s purchase price in closing costs.

The typical VA loan costs are: appraisal, title charges, VA funding fee, and possibly discount points. Also, you may need to pay a credit report fee. Shop for the Best VA Mortgage Lenders offering competitive VA House Loans for people in the Air Force, Army, Navy, Marines, Coast Guards, Reserves, etc.

The VA home loan is a great finance vehicle for those who have previous military service.

It is really the premium finance choice if you qualify for the government endorsed program.

The reason is that the VA loan benefits and qualification criteria are so generous.

What Are VA Loan Benefits:

Numerous advantages accompany the VA loan benefit, a program meticulously crafted to recognize and support our nation’s servicemembers. The VA guarantees zero down home loans for first time buyers. Some of these VA loan benefits encompass:

- Reduced VA loan rates

- zero down payment requirement

- No PMI (private mortgage insurance)

- Access to VA cash out refinance program

- Higher debt-to-income ratio allowances

- Assistance with closing costs, with the potential for seller concessions of up to 4% of the purchase price, which your real estate agent can skillfully negotiate

- No early repayment penalty fees

If you have a desire to buy a home using a VA loan benefit, we will help you find an experienced VA lender. We comprehend the distinct needs of servicemembers and their families and can guide you in seizing the VA loan benefits you’ve rightfully earned.

FAQ for VA Home Loans

Who qualifies for a VA loan?

Eligibility for a VA loan option is available to veterans, active-duty service members, reservists, and surviving spouses. To qualify, applicants must meet specific service requirements set by the Department of Veterans Affairs and obtain a Certificate of Eligibility (COE), which verifies their eligibility status. The COE can be acquired through the VA’s eBenefits portal, a lender, or by mail, ensuring applicants meet the necessary conditions to access this home loan benefit.

How do I apply for a VA loan?

You can apply for a VA loan through VA-approved lenders by submitting your Certificate of Eligibility (COE) along with the necessary financial documents, such as income statements and credit information. Many VA lenders use the Web LGY system to streamline the process, allowing them to quickly obtain COEs on behalf of borrowers, reducing delays and simplifying the application process on VA loans. (VA.gov, 2026)

What credit score do I need for a VA loan?

The VA does not set a minimum credit score requirement, but most lenders prefer a score of at least 620. Individual lenders may have stricter requirements depending on loan terms and borrower history. Keep in mind that there is actually no minimum credit score for VA loans, so if you have below average credit and are eligible for a VA loan, you need to find the right lender.

Can I Get a VA Loan with a Manufactured or Mobile Home?

Many military borrowers want to know if they can get a VA home loan for mobile home. Yes and know. If you have a mobile home that was converted to a manufactured house and meets the VA specifications it is possible. Many borrowers have gotten a VA loan manufactured home financing. Make sure when you are shopping VA home lenders that you verify they do VA loans on manufactured or modular homes.

Do you have to be active duty to get a VA loan?

No, active-duty status is not mandatory to qualify for a VA loan. Veterans, certain National Guard and Reserve members, and some surviving spouses may also be eligible, provided they meet specific service and discharge criteria. Obtaining a Certificate of Eligibility (COE) is essential to confirm qualification.

What are the occupancy requirements for a VA loan?

Borrowers are generally required to occupy the home as their primary residence within 60 days of closing. However, exceptions may be made for service members on active duty, allowing them additional flexibility if deployment or other military obligations prevent immediate occupancy. In such cases, a spouse or dependent may fulfill the occupancy requirement on the borrower’s behalf.

Can I use a VA loan to purchase an investment property?

VA loans are intended for primary residences only. However, buyers can purchase multi-unit properties (up to four units) if they occupy one as their primary home (Military.com, 2025)

What is a VA Streamline Refinance?

Can I get a National Guard VA loan?

Yes, National Guard members may qualify for a VA home loan. Eligibility typically requires at least six years of service in the Guard, or 90 days of cumulative active-duty service under Title 32 orders, with at least 30 consecutive days. A Certificate of Eligibility (COE) is necessary to proceed.

Can a non-veteran assume a VA loan?

Yes, a non-veteran can assume a VA loan if the original loan was closed before March 1, 1988, or if the lender and VA approve the assumption. The new borrower must meet credit and income requirements. However, the veteran’s VA entitlement remains tied to the loan unless the buyer is a qualified veteran who substitutes their entitlement.

What is a 100 percent disabled veteran home loan?

A 100 percent disabled veteran home loan refers to a VA-backed mortgage with enhanced benefits for veterans rated totally disabled. These include exemption from the VA funding fee, eligibility for property tax exemptions in many states, and access to VA zero-down payment financing. It provides more affordable homeownership options for qualifying disabled veterans.

What is the VA funding fee?

The VA funding fee helps sustain the VA loan program and varies based on loan type and borrower status. First-time users pay 2.15% to 3.3%, while subsequent users may pay a higher interest rate.

Can I use a VA loan more than once?

Yes, you can use a VA loan multiple times as long as you meet the eligibility requirements for each new loan. However, only one active VA loan is typically allowed at a time, unless you qualify for a second entitlement. This second entitlement can enable you to take out another VA loan while still holding an existing one, often used when relocating or purchasing a second home due to a change in duty station or family needs. As long as the loan remains within the VA loan guidelines, you can access this benefit repeatedly throughout your lifetime.

Can you have two VA loans at the same time?

Yes, it’s possible to have two VA loans simultaneously under certain conditions. This often occurs when a veteran relocates but wants to keep the first home. The second loan depends on remaining VA entitlement and meeting occupancy and lender guidelines.

How long does it take to assume a VA loan?

Assuming a VA loan typically takes 30 to 60 days, depending on the lender’s processing time and the buyer’s eligibility. The process involves credit approval, VA forms, and legal paperwork. Once approved, the new borrower assumes the loan’s current balance, interest rate, and terms.

Can you use a VA loan to buy land?

VA loans generally do not cover the purchase of raw land alone. However, they can be used to buy land if it’s combined with a construction loan for building a primary residence. The land and home must meet VA property standards and be intended for owner-occupancy.

Do I need PMI with a VA loan?

No, VA loans do not require private mortgage insurance (PMI), regardless of the down payment. Instead, borrowers pay a one-time VA funding fee, which helps support the program. This benefit can significantly lower monthly mortgage payments compared to conventional loans.

How long do you have to serve in the military to get a VA loan?

Service requirements for a VA loan vary:

- Active-duty members: At least 90 continuous days during wartime or 181 days during peacetime.

- National Guard and Reserve members: Six years of service, or 90 days of cumulative active-duty service under Title 32 orders, with at least 30 consecutive days. These requirements may differ based on service dates and discharge status.

The Bottom Line on VA Home Loan Financing

A VA home loan is one of the best benefits today of military service once you get home. You can get a loan with no money down, no mortgage insurance and a very low interest rate. It also is easy to qualify for a VA home loan.

If you are a military vet or current military, you should see if you can qualify for a VA loan before you consider any other mortgage product.

Last reviewed: March 23, 2026 by Bryan Dornan, Mortgage Lending Expert and Founder of RefiGuide.org. VA funding fee rates sourced from VA.gov funding fee and closing costs page (rates effective April 7, 2023, through November 14, 2031). Loan limits sourced from FHFA conforming loan limit announcement November 25, 2025 (effective January 1, 2026). Rate data sourced from Freddie Mac PMMS March 19, 2026; Navy Federal Credit Union rate sheet March 2026.

About Bryan Dornan

Bryan Dornan is a financial journalist and mortgage industry veteran with nearly 30 years of experience as a lender, loan officer, mortgage broker, and chief marketing officer. He currently serves as Chief Editor of RefiGuide.org, where he has built one of the most trusted mortgage education platforms in the United States. Bryan has founded multiple mortgage and digital marketing companies throughout his career and remains focused on helping homeowners leverage home equity wisely while making affordable homeownership accessible to everyday Americans. He is a licensed California Real Estate Broker DRE: #01203791. and writes for RealtyTimes, Patch, Buzzfeed, Medium and other national publications. Find him on Twitter, Muckrack, and Linkedin

More articles by Bryan Dornan