With the Federal Reserve lowering rates, you should consider refinancing your home equity loan or HELOC for a lower payment. With inflation soaring, it makes sense to maximize lower monthly payments and refinance home equity loans for a better interest rate.

- Refinance Home Equity Loan for a Lower Monthly Payment

- Refinance for a Better Home Equity Rate

- Home Equity Loan Refinancing for More Cash Out

- Refinance Home Equity Line of Credit into a Fixed Rate

If you are ready to apply or have questions, the RefiGuide will help you shop with the best home equity professionals in the business.

The Home Equity Loan Refinance Could Save You Money and Get You More Cash Back!

Do you own your home and dream of rehabbing it?

Perhaps you want to pay off credit card debt with a 2nd mortgage or pay for your child’s college tuition.

But refinancing your first mortgage and pulling out cash doesn’t always make sense.

After all, interest rates are still high in 2025. With property values also elevated, many homeowners choose to access their equity with home equity loans.

The equity home loan allows homeowners to tap some of their equity without selling the home. But what happens if interest rates drop?

Can you refinance a home equity loan? Can you refinance into a lower monthly payment while getting more cash back? Keep reading to learn all about home equity loan refinancing. If you would like to refinance with home equity loan programs than you will be interested in the new lending possibilities.

What Is a Home Equity Loan Refinance Program?

A home equity refinance loan refinance is usually a fixed-rate second mortgage that allows homeowners to take some of their home equity in cash. Most 2nd mortgage lenders allow you to to refinance a HELOC or home equity loans and take additional cash out up to 80% or 85% of a home’s value, including what is on the first mortgage.

In most cases in 2025, the refinance equity loan has a lower rate than most credit cards and personal loans, and is usually for five or 10 years.

An equity home loan’s rate doesn’t usually change and you know what you will pay every month until it is paid off. The money is received in a lump sum, which is different than a home equity line of credit or HELOC. This secure credit line where you can take money out as you wish, up to your approved limit.

Best Practices for Refinancing a Home Equity Loan in 2025

Many homeowners like home equity loans because the rate is fixed, meaning you have predictable payments for the life of the loan. 2nd mortgage interest rates could fall in 2025 and 2026, so can you refinance your home equity loan for a lower rate?

Yes. Just like a first mortgage, you can refinance home equity loans. This is often a good choice if rates have fallen by at least .5% or 1% since you got the loan. Refinancing the loan also could be a good idea if you had an adjustable rate and want to switch to a fixed rate loan.

- Compare the proposed cash out refinance to your existing mortgage payment plus the new home equity loan payment and see which option is more cost-effective.

- If you are refinancing an original home equity loan, verify you have improved terms and lower interest rates.

- Compare the new monthly payment with a cash out refinance versus home equity loan payment

- Verify with your lien holder that you are allowed to get a new home equity loan that subordinates behind your primary mortgage

- Make sure you know how much home equity you need to qualify and meet the LTV requirements

- Compare the loan terms and repayment periods from competitive home equity loan lenders

- Verify the underwriter approved the loan proceeds being allowed for home improvements, debt consolidation, investment property, etc.

- Shop and compare closing costs and refinance home equity loan rates before signing paperwork.

When you refinance you pay off the mortgage and replace it with a new loan. When you refinance a home equity loan, you are paying off the original mortgage balance or home equity line and replacing it with a new second mortgage or HELOC. If you are refinancing a HELOC, you will be eliminating the variable interest only payments and converting it into a fixed interest rate loan with a fixed monthly payment.

How Much Does It Cost to Refinance a Home Equity Loan?

Refinancing a home equity loan typically costs 2% to 5% of the loan amount. Common fees include application fees, appraisal fees, origination fees, and title costs. Some lenders offer no-closing-cost options, but these may come with higher interest rates. Shopping around and negotiating with lenders can help reduce home equity loan refinancing costs and make the process more affordable.

However, some lenders offer no-closing-cost refinance options, though these may come with slightly higher interest rates. The no closing cost HELOCs are very popular with homeowners looking to set up a line of credit in case of emergency. Shopping around and negotiating with lenders can help you minimize fees. Additionally, some banks waive certain costs for existing customers or those with strong credit profiles.

The total cost of home equity loan refinancing depends on your loan balance, credit score, and lender terms. Before refinancing, compare offers, calculate potential savings from a lower interest rate, and consider how long you plan to stay in the home to determine if refinancing is financially beneficial.

What Do You Need to Qualify to Refinance a HELOC or Home Equity Loan?

Before you try to get a new home equity loan with a lower rate, you should know what the potential requirements are.

That way, you can review your financial situation and get ready for applying:

• You generally need at least a 620-credit score to get approved for a home equity loan.

However, having a credit score of at least 700 will usually get you the best rates.

• You will usually need to have at least 20% equity in the property to get a 2nd mortgage.

Lenders want you to have a stake in the property so you can pull out cash.

• Lenders typically want to see a debt-to-income ratio no higher than 43%.

This is the back-end ratio, which is a measure of all of your monthly debt payments compared to your gross monthly income.

• If you want to refinance to take advantage of lower rates, it will help to raise your credit score as much as possible.

If your credit score is under 700, you could have trouble qualifying for the best rates. Sometime the credit score requirements for HELOCs are different than fixed rate equity loans, so verify with the lender when shopping second mortgage options.

How Can I Lower the Mortgage Rate on My Home Equity Loan?

Refinancing a home equity loan entails substituting your current loan with a new one, possibly to obtain a reduced interest rate, modify the repayment term, or access additional equity resulting from your home’s appreciated value.

- Compare today’s pricing to your existing home equity loan rate.

- Factor in closing costs because if you roll them your loan amount will increase.

- Compare your current monthly payments to the proposed new loan.

- Consider refinance home equity loan rates with fixed rate terms.

Ultimately, no one can precisely predict when mortgage rates will begin to drop. If the rates quoted by home equity loan lenders are unsustainable for you, it’s wise not to proceed with the assumption that you can refinance later. The timing is uncertain, and in the interim, you risk losing your home if you cannot keep up with the monthly payments. Therefore it is prudent to refinance your home equity loan if you have the ability to save money with lower monthly payments and or improve your terms. Search for the best home equity loan rates online.

Can I Refinance a Home Equity Loan for a Better Terms?

Another option is to refinance to a home equity loan with a different term length, either longer or shorter, depending on whether your aim is to decrease your monthly payments or expedite loan repayment. Additionally, if you possess surplus equity in your home, you have the opportunity to refinance into a larger home equity loan amount, enabling access to additional cash.

- Refinance an Equity Loan into a Lower Interest Rate

- Convert Adjustable Rate HELOCS into a Low Fixed Rate Home Equity Loans

How Much Does It Cost to Refinance a Home Equity Loan?

Closing costs for home equity loan refinancing typically range from 1.5% to 5% of the loan principal.

For instance, if you’re refinancing a HELOC or equity loan with a balance of $50,000, anticipate paying between $750 and $2,500.

So if the closing costs were $750, you would need to borrow at least $50,750 if you wish to roll the home equity loan closing costs into the new loan.

Similar to first mortgage refinancing incurs standard fees, including processing, underwriting, notary, appraisal, title, escrow and origination fees.

Pros and Cons of Refinancing a Home Equity Loan

Like any financial decision, deciding to refinance a home equity loan should be considered carefully before making the final call. Here are the pros and cons of refinancing your home equity loan:

Pros

First, you can potentially lower your monthly payment, assuming you qualify for a lower interest rate. Having a lower rate could allow you to save considerably on interest over the years.

Second, you can refinance your loan into a longer or shorter repayment term. Switching to a longer term will reduce the payment but will increase interest payments. You also could select a shorter term, which increases monthly payments but reduces interest.

Cons

First, you may have a prepayment penalty for your current home equity loan. Some lenders may charge a prepayment penalty for paying the loan off before the end of the term.

Second, if you cannot keep up with the new payment schedule, you could lose the home to foreclosure.

Third, if your home decreases in value, you could owe more than the home is worth. This makes it more difficult to sell the home. During the mortgage crash of 2008, many people owed more than their home was worth and were stuck paying the mortgage on an underwater property.

What About Refinancing a Home Equity Loan Into a HELOC Line of Credit?

People frequently ask us if they can refinance a home equity line of credit. So many borrowers wonder if they can refinance their home equity loan into a HELOC. Yes! Refinancing into a home equity line of credit could be a wise decision if interest rates are falling. HELOCs usually have a variable interest rate and can be an economical choice when rates are dropping.

Another reason to consider refinancing into a HELOC is greater flexibility. A HELOC is a line of credit that you can pay off and reuse as you like. Many homeowners like the flexibility and reusability of a HELOC loan.

Many homeowners want to convert their credit line and refinance into a fixed-rate home equity loan: Most HELOC loans have variable rates, meaning the interest rate fluctuates with market conditions. When the interest rates are rising, we suggest refinancing into a fixed-rate home equity loan that includes paying off your HELOC to avoid higher future interest payments.

However, remember that a HELOC comes with a variable interest rate. Your borrowing costs could rise significantly if interest rates rise. Also, a HELOC has flexible payments so the lender may have more stringent borrowing requirements. Compare a HELOC vs Home Equity Loan.

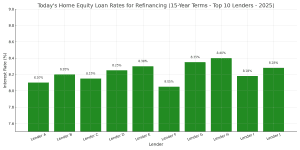

Top 5 Lenders for Home Equity Loan Refinance Offers in 2025

In 2025, refinancing a home equity loan can be a strategic move to secure better terms, lower interest rates, or consolidate debt. Here are five top lending sources offering competitive home equity loan refinance options:

-

Navy Federal Credit Union

Ideal for military members and their families, Navy Federal allows borrowing up to 100% of home equity with no closing costs or origination fees. -

Rocket Mortgage

Offers a high LTV 2nd mortgage program up to 90% loan-to-value (LTV) with a minimum credit score of 680. Known for a fully online application process and quick funding. -

LoanDepot

Provides premier equity loans with no closing costs, fixed APRs, and loan amounts from $35,000 to $500,000. LoanDepot utilizes a data-based approach for property valuations, eliminating the need for a traditional appraisal. -

PNC Bank

Recognized for its comprehensive home equity financing, PNC Bank provides flexible terms and competitive rates, catering to a wide range of borrower needs. -

RefiGuide.org

As a resource platform, RefiGuide.org assists borrowers in finding the best home equity lenders tailored to their specific needs, connecting users with suitable lenders without any cost or obligation. (not a lender but free service to connect consumers with banks, credit unions and lenders online.)

When considering refinancing your home equity loan, it’s essential to compare offers from multiple lenders to find the best fit for your financial situation. Factors such as home equity interest rates, terms, closing costs, annual fees, and eligibility requirements should be carefully evaluated.

Common Questions and Answers:

Can You Negotiate Better Rates When Refinancing a Home Equity Loan?

An additional approach to potentially secure improved rates and terms for your home equity loan or HELOC is through negotiation. After receiving a quote from the broker or lender, they might be consider negotiating, particularly if you have an existing relationship with the institution. To bolster your negotiation position, obtain alternative offers from other credible home equity lenders.

Cash Out Refinance Versus Home Equity Loans

In many ways these types of mortgages accomplish the same thing, Both are secure loans that offer cash back in the loan, but the cash out refinance is a first mortgage and the equity loan is considered a 2nd mortgage. This is important because if you already have a low first mortgage rate and you choose a cash out refinance, then you will have a higher interest rate to receive the cash back.

If you get cash from the home equity loan, you can keep your existing low interest home mortgage. In this kind of market, the home equity loan refinance offers you the best of both worlds. Get cash out from an equity loan and keep the great interest rate that you already have locked, down.

Can I Refinance My Home Equity Loan into My Mortgage?

One of the most common questions we get is, “Can you refinance a mortgage and home equity loan?” Certainly, it’s possible to refinance an equity loan or HELOC into a first mortgage. This can be accomplished either by choosing for a cash-out refinance and utilizing the funds to clear the line of credit or by consolidating the remaining balance from the HELOC into refinance mortgage of your home’s primary mortgage. In this current market it rarely makes sense, but it is possible. Let’s say you have a first mortgage rate over 6%, then refinancing your first and second mortgage together for one new mortgage makes sense.

How Long Does It Take to Refinance a Home Equity Loan or HELOC?

Refinancing your HELOC or home equity loan offers the opportunity to lock a lower interest rate, adjust your term, consolidate debt, or access cash from your equity. The timeframe for how long a it takes to close on an equity loan will vary depending upon what type of appraisal you need, how much income documentation needs to be reviewed and how long the home equity loan lenders may take. Nonetheless, the majority of home equity loans and credit lines typically close within 30 to 45 days from the application. If you the lender or broker waives the appraisal requirement, then it could speed up the process a few weeks.

Can I Get a Home Equity Loan from a Portfolio Lender?

There are many new programs for refinancing home equity loans this year. Private money and portfolio loan lenders have rolled out aggressive home equity products to meet the consumer demand for HELOCs and 2nd mortgages. If you have really good credit and no equity or pretty bad credit with lots of equity, then you may be a candidate for a portfolio home equity loan.

Can I Refinance if I Have a Home Equity Loan?

Yes, you can refinance your mortgage if you have a home equity loan, but the process can be more complex. Your home equity lender must agree to subordinate their loan, meaning they keep a secondary lien position behind your new mortgage. If they refuse, you may need to pay off the home equity loan first. A refinance can be beneficial if it lowers your interest rate or improves loan terms.

Can You Refinance a HELOC into a Home Equity Loan?

Yes, you can refinance a HELOC into a home equity loan. This can be a good option if you want to switch from a variable interest rate HELOC to a fixed-rate home equity loan with predictable payments. Refinancing may also provide better loan terms, especially if interest rates have dropped. However, eligibility depends on your credit score, home equity, and lender requirements.

Do You Lose Equity When You Refinance?

Refinancing does not directly reduce your home equity, but it can impact it depending on the loan terms. If you take cash out during the refinance, your equity decreases because you’re borrowing against it. However, if you refinance to a lower interest rate without borrowing additional funds, your equity remains the same and could grow faster with lower monthly payments.

Can I Borrow Against My Equity without Refinancing?

Yes, you can borrow against your home equity without refinancing by getting a home equity loan or a home equity line of credit (HELOC). These options allow you to access cash based on your home’s value without changing your existing mortgage. HELOCs provide a revolving credit line, while home equity loans offer a lump sum with fixed payments.

Can I Refinance My Mortgage with an Equity Loan?

No, a home equity loan is typically a secondary loan and cannot directly refinance your primary mortgage. However, you can use a home equity loan to pay down or pay off your mortgage, essentially replacing it with the home equity loan. This strategy may work if the home equity loan offers a lower interest rate, but it’s important to compare total loan costs and repayment terms.

Does It Make Sense to Refinance Your Home Equity Loan?

As with a first mortgage refinance, homeowners can refinance their home equity loan, if they qualify. You will need to provide all of your financial and credit information again, and the home may need a new appraisal.

Generally, the best reason to refinance a home equity loan is if rates have dropped significantly since you got the loan. Before refinancing, think about how long you will stay in the home and what your income situation looks like in the near and medium terms.

If you are ready to apply for a home equity loan refinance, our loan professionals can assist you. We will show you several options based on your financial and credit situation, so contact us today!

About RefiGuide

Bryan Dornan is a financial journalist and currently serves as Chief Editor of RefiGuide.org. Bryan has founded several mortgage and marketing companies and has worked as a loan officer and mortgage broker in the industry for over 25 years and has a wealth of experience in providing mortgage clients with the highest level of service in the industry. Bryan's continual focus is to promote affordable home-ownership to consumers like you across the United States. He also writes for RealtyTimes, Patch, Buzzfeed, Medium and other national publications. Find him on Twitter, Muckrack, and Linkedin

More articles by RefiGuide