American homeowners love home equity loans and many people have been inquiring about leveraging their second home or rental property with a HELOC or 2nd mortgage. Home prices seem to be leveling off with one major house price indicator at S&P finding prices up 3% from January last year. Thousands of homeowners have taken out a home equity loan or HELOC to finance the down-payment required to buy a rental, investment property or second home. The RefiGuide will connect you with rental property lenders and show you how to take out a HELOC on investment property or secure a second home equity loan in 2025.

Can I Take Out a Home Equity Loan on a Rental Property in 2026?

This is a blistering pace, especially when you consider this growth was on top of an 11% rise that was reported at the beginning last year.

More and more real estate investors are seeking a HELOC on investment properties.

Not All banks offer the HELOC to buy second home, but the RefiGuide can connect you to lenders that specialize in cash-out HELOCs to purchase a 2nd home or rental property.

Because of rising home equity, millions of homeowners wonder what they should do with their new-found wealth.

On average, the typical homeowner gained more than $25,000 in equity in the last few years.

There are many new home equity line of credit on second home products being rolled out in 2025, so this is a new opportunity for savvy homeowners.

Let’s consider the key points on leveraging home equity on second homes and investment properties in this current financing environment. The LTV and credit requirements may be slightly different on a HELOC to buy second home.

How to Get a HELOC or Home Equity Loan on a Investment Property or Second Home

One option for that cash is to pull out equity. But if you already own a 2nd home, vacation home, or rental property, you also may be able to pull that cash out. But with mortgage rates recently topping 6.5% for new and refinanced mortgages, you may not want to pull cash out with a refinance.

Getting approved to home equity loan on a second home is still possible this year. There are a few lenders that have eased the minimum credit score requirements for a home equity loan on rental property. The RefiGuide can match you with lending companies that offer competitive home equity loans on investment properties.

The new home equity loan guidelines have eased credit and equity requirements, so homeowners can once again consider an equity loan. Instead, consider getting a home equity loan on your second home or vacation property.

Now could be the perfect time because fixed rates for home equity loans are still much lower than for credit cards or personal loans. Our team can help you shop for the best HELOC lenders offering a home equity loan on an investment property.

The key is to find a mortgage broker or lender willing to offer you a HELOC or home equity loan on a rental or investment property. Most banks and credit unions will not offer home equity loans and HELOCs on a investment property pose a higher risk for lenders because second mortgages are more likely to go unpaid if the borrower encounters financial difficulties. This risk is even greater for a rental property if you already have mortgages on both the investment property and your primary residence. As a result, some 2nd mortgage lenders may impose stricter qualification requirements on borrowers.

- Home Equity Loans on Non Owner Occupied Homes OK

- Fixed Rate Home Equity Loan on Rental Property

- Revolving HELOC on Investment Properties OK

Why Get a Home Equity Loan on a Second Home?

Some homeowners like the idea of taking cash out of a second home. That way, you are not removing equity from your primary residence. Using the vacation home or investment property for the home equity loan reduces the chances of being underwater on your property.

Luckily, many lenders these days offer home equity loans and other 2nd mortgages on second homes. Getting the loan may be more complex than if you attempt to refinance a home that you don’t live in. But that doesn’t mean it’s impossible to enjoy the low interest rates of a 2nd mortgage loan! You can!

What Are the Rules for Taking Out a Home Equity Loan on a Rental Property or Second House?

Taking out a loan on a second home, vacation home, or rental property you don’t reside in is a higher risk for the lender.

So, you should expect a higher interest rate and stricter lending rules for your home equity loan.

But do not worry, with enough planning, you will be able to qualify for your second mortgage.

Typically, getting a home equity loan on a second home requires putting down at least 10 percent. More is better because you will get a lower interest rate. That doesn’t affect getting a home equity loan on the home, but just FYI!

Also, you probably need to leave 25% or more of the equity in the second home. That means you need quite a bit more equity than 25% to make the home equity loan worth doing.

Credit score requirements are also higher for second homes and the DTI limits are stricter.

More on requirements for credit lines and home equity loans on a second home:

- You need to own the property for at least a year

- Credit score of approximately 680 to 700 (or lower LTV)

- Larger down payment and a lower home to value ratio or LTV

- Restrictions on where the property is located

While there are stricter requirements, you’ll be happy to know getting an equity loan on a second home is easier than for an investment property. So, you should be able to find lenders offering more 2nd mortgages on the vacation home if you have one.

Home Equity Loan on Investment Property Opportunities

Successful real estate investors utilize various tools to skillfully navigate and seize new opportunities. One such tool is home equity loans, which, while commonly used by homeowners for their primary residences, can also benefit real estate investors.

Although obtaining home equity loans on investment properties can be challenging, pragmatic real estate investors can leverage this tool to cover expenses, address shortfalls, or even finance the buying additional investment and rental properties.

We will show you how to use home equity for a down payment on a second home or investment property.

Does a HELOC have to be on a Primary Residence?

Most home equity loans and HELOCs are secured against primary residences, as mortgage bankers tend to favor loans tied to the borrower’s primary dwelling, assuming that repayment will be prioritized. Nonetheless, certain lenders extend 2nd mortgages and HELOCs to investment properties as well.

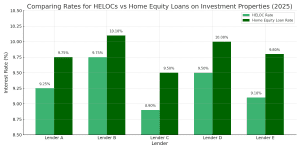

Current Interest Rates for Home Equity Loans on Investment Properties

As of April 2025, interest rates for Home Equity Lines of Credit (HELOCs) and home equity loans on investment properties are generally higher than those for primary residences. This is due to the increased risk lenders associate with investment properties.

Current Interest Rates:

-

HELOCs: The national average interest rate for HELOCs is approximately 7.94%, based on Bankrate’s latest survey.

-

Home Equity Loans: The national average interest rate for home equity loans stands at around 8.36%.

It’s important to note that these rates can vary based on factors such as credit score, loan-to-value ratio, and the specific lender’s policies.

When considering tapping into your investment property’s equity, it’s crucial to compare offers from multiple lenders, taking into account the interest rates, fees, and terms they provide. Additionally, ensure that the lender allows for equity loans or HELOCs on investment properties, as some may have restrictions.

If you need further assistance or personalized recommendations based on your specific situation, feel free to ask!

Can You Get a HELOC on Investment Property?

Yes, it’s possible to get a home equity line of credit or HELOC on investment property, but it tends to be more challenging and expensive compared to obtaining a HELOC on a primary residence:

- Approval Requirements: Lenders have stricter criteria for HELOCs on rental properties, and many don’t offer them.

- Interest Rates: HELOCs on rental properties usually come with higher interest rates than other loan types.

- Debt-to-Income Ratio: Lenders often limit the debt-to-income (DTI) ratio for rental property HELOCs to 40–50%, though this can vary between 35–55% depending on the lender.

- Cash Reserves: Lenders typically require significant cash reserves, often at least 18 months’ worth.

- Rental Income History: A documented rental income history is usually required.

A HELOC on a rental property can be a smart financial choice if you need funds for real estate-related expenses, such as, property improvements or capital repairs. Some borrowers take out a HELOC to pay off the mortgage on another investment property. Ask about the new HELOC for non-owner occupied borrowers.

Of course, in most cases you need strong credit, sufficient equity, and proof of rental income. These HELOCs are ideal for property improvements or leveraging equity to expand your real estate portfolio.

Top Lenders for Investment Property Home Equity Loans

-

Connexus Credit Union: Offers both HELOCs and home equity loans with competitive rates and flexible terms.

-

U.S. Bank: Provides HELOCs with high loan amounts and options suitable for investment properties.

-

Navy Federal Credit Union: Caters to military members and their families, offering both HELOCs and home equity loans with favorable terms.

-

PNC Bank: Recognized for its overall offerings in home equity lending, including options for investment properties.

-

LoanDepot: Known for fast closing times and offering HELOCs suitable for various property types, including investment properties.

Can I take a home equity loan on an investment property?

Yes, it’s possible to take a home equity loan on an investment property, though fewer lenders offer them compared to primary residences. Of course, terms are often more conservative, requiring higher credit scores, larger equity, and lower loan-to-value ratios. If approved, a fixed-rate home equity loan can provide money upfront for renovations, debt consolidation, or new real estate acquisitions.

Can you take out a HELOC on an investment property more than once?

Yes, there is No limit on how many properties you can take a HELOC or equity loan out on. You are not limited t one HELOC on one rental property. Some savvy real estate investors even use the the HELOC funds as a down payment on another rental property. For example, if you owned ten investment properties you could take out a home equity line of credit on ten different properties.

Can I use a HELOC for a down payment on an investment property?

Yes, as we mentioned earlier, you can use a HELOC from your primary residence to fund the down payment on an investment property. This strategy allows you to leverage existing equity without liquidating other assets. However, lenders will consider the HELOC payment in your debt-to-income ratio, so ensure your finances support both obligations. It’s a common method used by real estate investors.

What About a Cash-Out Refinance on a Second Home?

There are stricter requirements, but you don’t have to necessarily be locked into one type of loan to get access to the cash you want. You also could consider a home equity line of credit or cash-out refinancing. Which loan option is best depends on your situation and financial goals. Read more about cash out refinance requirements on investment properties.

Consider an Equity Loan If…

As we explained earlier, first mortgage rates for new purchases and refinances are higher than they have been in several years. With rates recently exceeding 5%, you may not want to refinance your second home to pull out cash.

It is probably better in this rate environment to get a home equity line or HELOC to pull out your money. Also, a 2nd-mortgage doesn’t require you to restart the payment period and increase how long you pay your mortgage. This also extends how long you pay interest, which could save you thousands of dollars over the long term.

Whether you should get a credit line or HELOC depends on several factors. Let’s take a look:

- Get a home equity loan if you prefer taking a large chunk of equity out of the second home at one time. You will pay the money back at a fixed interest rate over a set period, usually 20 or 30 years.

- Consider a home equity lines of credit if you want to pull the money out over time. You can access as much as you want up to your credit line at any time. Also, repay the money over time and the credit line can be accessed again, just like a credit card. You have an interest only draw period, then a repayment period paying principal and interest. HELOCs also offer interest only payments that increase your cash flow with lower monthly payments during the draw period.

Whether you get a home equity loan or HELOC, you will have two monthly payments, so make sure you have the money and organization to make that happen.

Why Are There Different Lending Rules for 2nd Homes?

If you were buying and selling real estate before 2008, you probably remember it was easier to pull cash out of first homes and even second homes. But after the mortgage crash of 2008 and 2009, lenders realized lending guidelines were lax and that led to too many defaults.

In 2025 getting a HELOC on second home will be easier for borrowers to obtain than previous year because more banks and lenders are rolling out new home equity programs.

Instead of getting a second home mortgage with 100% or even 105% of your home’s equity with loose credit rules, lenders weren’t even offering second mortgages on second residences. Unlike your primary home, home loans for second homes are a higher risk for the lender.

Also, second mortgages are always a higher risk for the lender. This is because the loans are in the ‘2nd lien’ position, meaning they may get paid less or slower if you default. For these reasons are why getting a second mortgage on a second home is more difficult today. And you will pay a higher interest rate.

Can I Deduct the Interest Paid on a HELOC for an Investment Property?

Interest paid on your rental property HELOC or home equity loan might be eligible for tax deduction, potentially lowering your taxable income. However, to qualify for this deduction, the loan must be utilized for property improvements. You should talk to an experienced tax consultant that understands your specific situation. Whether you need a HELOC or home equity loans on investment properties, the RefiGuide can help you find the best brokers and lenders in the business.

How long does it take for a home equity loan?

The timeline for obtaining a home equity loan typically ranges from 2 to 6 weeks. The process includes submitting an application, underwriting, a property appraisal, and final approval. Delays can occur if documentation is incomplete or the appraisal process takes longer than expected.

Can I get a non owner occupied HELOC?

Yes, when you get a HELOC on an investment property you are taking out a home equity line of credit on non owner occupied residence. As we mentioned before the HELOC rates on investment properties is a little higher but this financing vehicle is a valuable tool for real estate investors.

How much equity can you take out of an investment property?

Lenders typically allow you to access up to 70% to 75% of your investment property’s appraised value through a cash-out refinance. This means you must retain at least 25% equity in the property. For example, if your property is valued at $500,000, you could potentially cash out up to $375,000, minus any existing mortgage balance. So if your investment property is worth $500,000 and your first mortgage balance is $300,000 you could take out a HELOC up to $75,000.

What banks offer HELOCs on investment properties?

Several financial institutions offer Home Equity Lines of Credit (HELOCs) on investment properties, including Wells Fargo, CitiBank, Chase, FlagStar, Bank of America, U.S. Bank and multiple credit unions. The non-owner occupied HELOC availability and terms may vary, so it’s advisable to contact these lenders directly to discuss your specific needs and eligibility.

How can I pull equity out of a rental property?

To access the equity in your rental property, you can consider a cash-out refinance, which involves replacing your existing mortgage with a new, larger loan and receiving the difference in cash. Alternatively, some lenders offer HELOCs on investment properties, allowing you to draw funds as needed up to a certain limit. Each option has its own requirements and implications, so it’s important to consult with lenders to determine the best fit for your situation.

How long do you have to own an investment property to do a cash-out refinance?

Lenders typically require a seasoning period before allowing a cash-out refinance on an investment property. This period usually ranges from 6 to 12 months, depending on the lender’s policies and the loan type. It’s essential to verify the specific seasoning requirements with your chosen lender.

Can I use Cash Out from a Home Equity Loan to Invest in a Real Estate Investment Trust?

Yes, you can use the money from a home equity loan or HELOC to invest in a real estate investment trust, also known as, REIT. However, we suggest being careful, as going into debt to make an investment can be risky. A home equity loan is a type second mortgage, that is secured to your property. Therefore it is crucial not to overleverage your finances without a clear understanding of the potential return on the borrowed funds. You are allowed to use a HELOC to write a check for real estate investments.

Why are home equity loan and HELOC rates higher on Investment properties?

HELOC rates for investment properties are typically higher than those for a primary residence. You can generally expect to pay an additional 0.5% to 0.75% above the current home equity loan rates. The same applies to home equity lines of credit on second homes, so it’s important to compare offers from multiple lenders to secure the lowest possible rate. We continue to hear about trusted banks lowering investment property HELOC rates for qualified borrowers. We will help you shop for the best HELOC lenders for investment property offers.

What banks offer a HELOC on investment property?

Loan Depot, TD Bank and US Bank are a few of the popular mortgage companies and banks that offer HELOCs on investment properties. Take advantage of our system that will show you banks that offer home equity loans on rental properties. The RefiGuide will help you shop from banks and lending shops that offer the best home equity loans and HELOCs on investment properties. Our team will help you find who offers a 2nd mortgage on investment property opportunities.

Can I use a HELOC to buy investment property opportunities?

Yes, you can use a HELOC to buy investment property opportunities. A HELOC allows you to access your home’s equity as a flexible line of credit, which can be used for down payments, renovations, or even full property purchases. However, ensure you can manage repayments and evaluate potential risks before proceeding. Using a HELOC to purchase investment property options has become a stealth choice for savvy homeowners.

Takeaway on Home Equity Loans on Investment Properties

Let’s remember that home equity loans can be a valuable tool for real estate investors. However, it’s important to carefully consider various factors to determine if it’s the right time to use this option. There are many benefits why you should choose a home equity loan on a second home or rental property over other financing options.

- Find the Best Home Equity Loan for Investment Property Options

- Flexible HELOC on Second Home

- Home Equity Line of Credit on Rental Properties

- Home Equity Loan on Second Property

- Low Intro Rate 2nd Home HELOC Programs

- Equity Loans Allowed on Multi-Family Residences

Taking out a home equity loan on a rental property or investment home can be a pragmatic move to free up cash-flow for real estate investors. Many savvy homeowners also get a HELOC on second home set up for home renovation, debt consolidation or in case of an emergency.

Generally, using a home equity loan to buy an investment property or second home is most effective when the funds are used for a cash offer. The lump-sum proceeds from your home equity loan or HELOC might cover the entire purchase price or supplement other assets, helping you reach the necessary amount.

You have the option to obtain a HELOC on a second home, granted you adhere to the lender’s criteria. This implies that you are not obligated to sell your vacation property to leverage the equity it has accumulated. Instead, you can access the value of a second home through methods such as a cash-out refinance, home equity loan, or HELOC line of credit.

If you already own a second home and want to access equity to pay for a major expense, you may be able to do so with a HELOC or second mortgage. There are more credit requirements and stricter lending rules, but you can still access the cash you need with a second mortgage on your second home. So complete the quick quote form and the RefiGuide will connect you with experienced mortgage lenders today so you can get started.

About Bryan Dornan

Bryan Dornan is a financial journalist and mortgage industry veteran with nearly 30 years of experience as a lender, loan officer, mortgage broker, and chief marketing officer. He currently serves as Chief Editor of RefiGuide.org, where he has built one of the most trusted mortgage education platforms in the United States. Bryan has founded multiple mortgage and digital marketing companies throughout his career and remains focused on helping homeowners leverage home equity wisely while making affordable homeownership accessible to everyday Americans. He is a licensed California Real Estate Broker DRE: #01203791. and writes for RealtyTimes, Patch, Buzzfeed, Medium and other national publications. Find him on Twitter, Muckrack, and Linkedin

More articles by Bryan Dornan