Wondering whether you should get a Fannie Mae cash-out refinance into a new mortgage with great interest rates and money coming directly to you? Check out our detailed guide to learn all the ins and outs of such a Fannie Mae cash out refinance mortgage. Fannie Mae continues to offer the most competitive rates for cash out refinancing in 2026 and the RefiGuide will enlighten you on the benefits and cash out guidelines from top FNMA lenders.

- Best Rates for Cash Out Refinances

- No Closing Cost Cash Out Refi Options

What Is a Cash-Out Fannie Mae Refinance Loan?

Fannie Mae has been buying and securitizing mortgages since the 1960’s.

The Fannie Mae cash out refinance is a program. Refinancing a home involves replacing the current mortgage with a new one with unique terms.

With a cash-out refinancing, you can turn the equity in your home into cash.

In such a scenario, your current loan is replaced with a new one by paying off the remaining mortgage balance and the difference is given to you as a lump sum cash.

In other words, you replace your existing mortgage with a bigger one and take cash based on your equity and your home’s current value.

Fannie Mae Cash Out Refi Frequently Asked Questions

Here are the top 12 Fannie Mae cash-out refinance questions commonly asked online for an FAQ section:

What Are the Eligibility Requirements for a Fannie Mae Cash-Out Refinance?

To qualify, homeowners must meet specific criteria:

- The property must have been owned for at least six months, with certain exceptions for inherited properties.

- The existing mortgage being refinanced must typically be at least 12 months old.

What is a limited cash-out refinance with Fannie Mae?

As implied by its name, the cash back awarded to a borrower is “restricted” — in accordance with Fannie Mae’s limited cash-out refinance guidelines, the sum cannot exceed 2% of the new loan balance or $2,000, whichever is lower.

How does a limited cash-out refinance differ from a cash-out refinance?

A limited cash-out refinance is akin to a no cash-out refinance, with the key distinction being that it permits you to roll your closing costs into your principal balance instead of paying them upfront at closing. Most lenders price the limited cash refinance, as if it were a rate and term refinance which merits .25 to .375 rate reduction in most cases.

Does Fannie Mae require reserves on cash-out refinance?

Six months’ reserves are required for the following scenarios: a principal residence transaction involving two to four units, an investment property transaction, and a cash-out refinance transaction with a DTI ratio exceeding 45%.

What is the difference between a Type 1 and Type 2 cash-out refinance backed by Fannie Mae?

In a Type 1 cash-out refinance, the loan amount of the new loan is either equal to or less than 100% of the payoff amount of the loan being refinanced. Conversely, in a Type 2 cash-out refinance, the loan amount of the new loan exceeds 100 percent of the payoff amount of the loan being refinanced.

What is the LTV limit for a Fannie Mae Cash Out Refinance Loan?

For single-family properties, the cash out refi LTV limit, also referred to as the loan-to-value ratio limit, is set at 80%. This implies that you must maintain a minimum of 20% equity in your home when opting for a cash-out refinance.

Does Fannie Mae offer a conventional cash-out refinance?

Yes, Fannie Mae offers a conventional cash-out refinance for homeowners who want to tap into their home equity. To qualify, borrowers typically need at least 20% equity, a minimum credit score of 620, and must meet debt-to-income (DTI) ratio requirements. The loan can be used for various purposes, including home improvements, debt consolidation, or major expenses. Borrowers must also meet six-month ownership seasoning requirements before applying. Checking lender-specific terms can help determine eligibility.

What are the Fannie Mae cash-out seasoning requirements?

Fannie Mae requires a six-month seasoning period before allowing a cash-out refinance. This means the borrower must have owned the property for at least six months before applying. Exceptions exist for inherited properties, legal settlements, or when a previous loan was part of a delayed financing transaction. Additionally, the loan-to-value (LTV) ratio and credit score requirements must meet Fannie Mae’s guidelines. Always check with lenders for specific eligibility and documentation requirements.

Is an Appraisal Required with FNMA Cash Out Refinances?

Yes, an appraisal is usually required to determine the property’s market value. The appraisal ensures that lenders correctly assess how much equity can be withdrawn.

How Does a Fannie Mae Cash-Out Refinance Differ from Other Refinance Options?

While other government-backed cash-out refinances, such as FHA or VA loans, may offer different terms, Fannie Mae’s refinance tends to offer competitive interest rates. However, it also comes with stricter qualification criteria, including maintaining specific equity levels and meeting ownership duration requirements.

Can the Cash Be Used for Other Investments?

Yes, the funds obtained from a cash-out refinance can be used for any purpose, including making a down payment on a new property or purchasing investment real estate.

What Are Fannie Mae’s Cash-Out Refinance Seasoning Requirements?

Under Fannie Mae Selling Guide Announcement SEL-2023-01, effective for all loans with note dates on or after April 1, 2023, the existing first mortgage being paid off must be at least 12 months old — measured from the note date of the existing loan to the note date of the new loan (Fannie Mae, 2023). Two exceptions apply: paying off existing subordinate liens and buying out a co-owner pursuant to a legal agreement are both exempt from the 12-month seasoning requirement. This rule doubled the prior 6-month standard and applies to all conventional cash-out refinances regardless of lender.

What Is a Limited Cash-Out Refinance Under Fannie Mae Guidelines?

A limited cash-out refinance (LCOR) under Fannie Mae guidelines is a refinance transaction where the borrower receives minimal cash proceeds — capped at the greater of 1% of the new loan balance or $2,000, following the SEL-2025-08 update effective September 27, 2025 (Fannie Mae, 2025). The primary purpose is to pay off the existing mortgage and finance closing costs into the new loan. Unlike a full cash-out refinance, the LCOR has no 12-month seasoning requirement — making it available sooner after purchase or a prior refinance. Review cash-out refinance rules and requirements for a full comparison of LCOR versus standard cash-out guidelines.

How Soon Can You Refinance a Fannie Mae Loan After Closing?

For a limited cash-out refinance, Fannie Mae imposes no minimum seasoning period — you can technically refinance the day after closing, though lenders may impose their own overlays. For a standard cash-out refinance, the existing first mortgage must be at least 12 months old from note date to note date under SEL-2023-01. For a rate-and-term refinance with no cash out, Fannie Mae’s Selling Guide does not specify a mandatory waiting period at the agency level, though individual lenders typically require 6 months. Review how often you can refinance a mortgage for complete program-by-program seasoning timelines.

Does Fannie Mae Consider Paying Off a HERO Loan as a Cash-Out Refinance?

No — this is a critical distinction. The HERO loan (Home Energy Renovation Opportunity) is a PACE loan — Property Assessed Clean Energy financing. Under Fannie Mae Selling Guide Section B2-1.3-02, paying off a PACE loan is specifically exempted from triggering cash-out refinance classification (Fannie Mae Selling Guide, 2026). A borrower paying off a HERO/PACE loan through a refinance can still qualify as a limited cash-out transaction — avoiding the 12-month seasoning requirement and the higher LTV restrictions that apply to standard cash-out refinances. This exception applies only to PACE debt used solely for energy-related improvements.

When Did Fannie Mae’s Cash-Out Refinance Guidelines Last Change?

Fannie Mae has made two significant cash-out guideline changes since 2023. SEL-2023-01 (announced February 1, 2023, mandatory from April 1, 2023) doubled the seasoning requirement from 6 months to 12 months for first mortgages paid off through cash-out refinances. SEL-2025-08 (effective September 27, 2025) updated the limited cash-out cash-back formula from “lesser of 2% or $2,000” to “greater of 1% or $2,000” — a borrower-favorable change on larger loan balances. To determine whether a refinance makes sense in 2026 given your specific rate and loan balance, use RefiGuide’s break-even calculator.

Can I Refinance and Cash-Out with My Mortgage?

You can refinance and cash out if you’ve built equity in your home.

It’s common for people to refinance their mortgage and take cash for significant expenses.

Whether that’s a good idea depends on your unique circumstances, current rate, and how it differs from the one you already have.

It’s a large financial undertaking, so you must consider all the nitty gritty details before deciding.

I will discuss everything you need to know about cash-out mortgage loans, including their requirements and pros and cons, so you can decide whether it’s a good move for you.

Government Cash-Out Refinance Types

Cash-out refinance mortgages can be roughly divided into two distinct categories: conventional and government-backed.

Banks and lenders offer conventional cash-out refinancing loans. The other type is also provided by banks or lenders but is backed by government agencies and has set conditions. Government-backed loans are typically more accessible, especially for individuals with low credit scores.

The government-backed cash-out refinance loans include:

- FHA Cash-Out Refinance: This type of loan is backed by the Federal Housing Administration and is available for individuals with a low credit score, with a loan-to-value (LTV) ratio of a maximum of 80 percent. You don’t have to have an existing FHA-backed mortgage to apply.

- VA Cash-Out Refinance: The Department of Veterans Affairs (VA) offers this refinancing option exclusively to eligible veterans, active-duty service members, and, in some cases, surviving spouses. It has the most flexible terms and can be applied with 100 percent LTV.

- USDA Cash-Out Refinance: The U.S. Department of Agriculture offers traditional refinancing loan for rural homeowners with USDA loans with no cash back. The USDA program does NOT offer a cash-out option, unlike other mortgage programs. If you wish to access your home’s equity, you’ll have to refinance using a different loan type, such as a Conventional, VA, or FHA loan.

How Does Cash-Out Refinancing Work?

A cash-out refinance mortgage uses the home as collateral. It is just like the mortgage you already have. The only difference is that you borrow more money by turning your home’s equity into cash.

That means that to refinance with a cash-out, you must have some equity in your home, typically at least 20 percent.

You’ll start the process by finding a lender (conventional or government-approved, depending on the type of refinancing). The lender will assess your current mortgage by examining how much you’ve paid and still owe. They’ll also conduct a home appraisal to estimate the value of your home and consider your creditworthiness.

Suppose your home is worth $250,000, and you’ve paid $100,000 already. That means you have $100,000 in equity. You can cash out this equity amount with the new mortgage minus any closing costs associated with the refinancing.

The new loan will have its own rate and term, which can be shorter or longer per your request or lender’s offer. Generally, homeowners prefer to refinance with a lower rate.

That said, a cash-out mortgage typically has higher rates than standard refinancing because it results in less or no equity for the homeowner, and the lender assumes all of the risk.

What Are the Requirements for Refinancing Mortgage with a Cash-Out?

To qualify for a cash-out mortgage refinancing, you must meet some basic requirements. The specifics vary by cash out refinance lenders, but knowing the minimum requirements will help you understand whether this is even an option for you.

Here are the cash out refinance requirements for conventional types:

Home Equity

As I mentioned, you must have built some equity in your home by paying off part of the mortgage. Most lenders require applicants to have at least 20 percent equity.

You can calculate it by subtracting the amount you still owe in the mortgage from the current appraised value. Also consider a home equity loan vs cash out refinance.

Credit Score

Your credit score is vital for a cash-out refinance loan because this is a bigger loan and essentially a new loan.

Lenders may set minimum credit score requirements for refinance applications. However, some lenders may also accommodate individuals with low credit scores, but they’re usually offered high interest rates. You can also use a co-signer who exceeds the minimum credit score requirements.

You can get the best cash-out refinance rates with a higher credit score, say 700 or above.

Debt-to-Income (DTI) Ratio

Your DTI is also important for lenders as it demonstrates your ability to make timely monthly payments. It’s the ratio of the debt you’ll owe and the pay you get every month.

Most lenders require a DTI of 45 percent or less. If your DTI is high, you may be able to satisfy the requirement with six months of reserves in your bank account.

Seasoning

The seasoning requirement stipulates that you must have owned the home for at least six months. The only exceptions are if you inherit or receive your home as a gift.

How Much Money Can You Get When You Refinance and Cash Out?

Lenders usually allow homeowners to borrow up to 80 percent of their home’s current appraised value with a cash-out refinance plan. Know that you don’t cash out this whole amount; you must use the funds from the new loan to pay off the existing loan.

Let’s say your home is worth $300,000, and you still owe $200,000 on a loan. Your LTV ratio is 67 percent, which is less than the maximum of 80 percent.

With the new mortgage, you can borrow up to $240,000 (80 percent of $300,000), of which $200,000 will go toward paying the original loan. You can cash out the remaining $40,000.

So, the maximum amount you can cash out is the difference between what you owe and your home’s current appraised value. Remember that other factors, such as the LTV and your credit score, are at play.

Benefits of Cash-Out Refinance Mortgage

Refinancing with a cash-out can offer several advantages:

- Lower interest rate: You can get a better rate with the new loan if the rates have dropped since your first mortgage or you’ve improved your credit score.

- Access to lump sum cash: With a cash-out refi, you can get a large amount of money, which can be (and should be) used for important expenses like consolidating debt, home renovation, or higher education.

- Tax advantage: If you’re refinancing with cash-out for home renovations, you can avoid paying taxes on the cash. See rules for tax deductions on cash out refinancing.

Drawbacks of Cash-Out Refinance Mortgage

- Bigger loan, less or no equity: Refinancing with cash-out results in you losing equity in your home. More importantly, it replaces your current loan with a bigger loan, which means more debt and likely decades of monthly payments, which may be higher than what you’re currently paying.

- Risk of losing your home: Your original mortgage carries the risk of losing a home, but this new mortgage increases that risk.

A cash-out refinance on your home can give you a large sum if you have equity. How much you borrow overall and how much you get in cash depends on several things, such as your home’s value, the current mortgage balance, your overall DTI, and your credit score.

I would only recommend refinancing with a cash-out if you’re getting a better rate and plan on using the cash for something important like home repairs or debt consolidation. If you have a good credit history and ample equity in your home, you can negotiate for a better rate.

Also, it’s best to cash out with only the amount you actually need. Taking on more debt than necessary while losing all equity in your home is not the best decision. Find Cash Out Refinance Investment Property Loans.

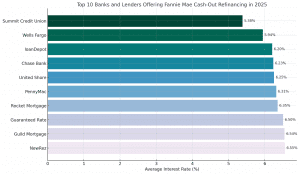

Top 10 Fannie Mae Lenders for Cash Out Refinancing in 2026

-

Summit Credit Union

-

Average Rate: 5.38%

-

Closing Costs: Low

-

Highlights: Offers competitive rates with minimal fees.

-

-

Wells Fargo

-

Average Rate: 5.94%

-

Closing Costs: Moderate

-

Highlights: Provides a range of refinancing options with nationwide availability.

-

-

loanDepot

-

Average Rate: 6.20%

-

Closing Costs: Moderate

-

Highlights: Known for its digital mortgage experience and quick processing times.

-

-

Chase Bank

-

Average Rate: 6.23%

-

Closing Costs: Moderate

-

Highlights: Offers personalized refinancing solutions with a strong customer service reputation.

-

-

United Shore Financial Services

-

Average Rate: 6.25%

-

Closing Costs: Low

-

Highlights: Provides competitive rates and efficient loan processing.

-

-

PennyMac

-

Average Rate: 6.31%

-

Closing Costs: Moderate

-

Highlights: Offers a variety of loan products with flexible terms.

-

-

Rocket Mortgage

-

Average Rate: 6.35%

-

Closing Costs: Moderate

-

Highlights: Known for its user-friendly online platform and quick approvals.

-

-

Guaranteed Rate

-

Average Rate: 6.50%

-

Closing Costs: Moderate

-

Highlights: Provides a streamlined digital mortgage process with competitive rates.

-

-

Guild Mortgage

-

Average Rate: 6.54%

-

Closing Costs: Moderate

-

Highlights: Offers personalized service with a variety of loan options.

-

-

NewRez

-

Average Rate: 6.55%

-

Closing Costs: Moderate

-

Highlights: Provides flexible refinancing solutions with a focus on customer satisfaction.

-

Note: Rates and closing costs are averages and may vary based on individual circumstances.

More Cash Out Refi FAQs

How long does a cash-out refinance take?

A cash-out refinance typically takes 30 to 45 days, depending on the lender, property appraisal, and document verification. Factors such as credit approval, home appraisal delays, and loan underwriting can impact the timeline. Borrowers can speed up the process by ensuring all required documents—including income verification, home insurance, and financial statements—are submitted promptly.

Is it smart to do a cash-out refinance?

It makes sense to refinance with cash-out if you can get cash at a potentially lower rate than a personal loan or credit card. It may also be worth it if you’re getting a lower rate than your previous mortgage. Remember that this would likely be a bigger mortgage spread out over decades, so it’s a big financial undertaking.

What is the cost of refinancing and cash out?

When refinancing a home with cash-out, you must bear the closing fees. Lenders typically charge an origination fee of 1 to 1.5 percent of the loan amount. Then, there are other costs like appraisal fees or credit check fees. The cost of refinancing can range from three to five percent of the loan amount.

What is the difference between a cash-out refinance and a home equity loan?

While both a cash-out refinance and a home equity loan allow the homeowner to borrow money using their home equity, there are significant differences. With a cash-out refinance, you replace your current mortgage with a new one, and you take the difference between the mortgage balance and the home value. On the other hand, a home equity loan is like a second mortgage, where you can borrow money equivalent to the equity in your home up to a certain limit.

How does cash out refinance affect basis of property?

A cash-out refinance does not directly affect the cost basis of a property for tax purposes. The cost basis is typically determined by the original purchase price plus capital improvements, such as renovations or structural additions. Since a cash-out refinance is a loan and not income, it does not increase or decrease the basis.

However, if refinance funds are used for home improvements, those costs may be added to the adjusted basis, potentially reducing capital gains taxes when selling the home. On the other hand, if the cash-out funds are used for personal expenses (e.g., debt consolidation, investments), they do not impact the property’s basis. It’s important to keep detailed records of how refinance proceeds are spent for future tax considerations. Consulting a tax professional is advisable.

- FNMA cash out seasoning

- cash out guidelines for Fannie Mae

Is a Cash-Out Refinance Taxable?

No, a cash-out refinance is not considered taxable income because it is a loan, not earnings. However, if you use the funds for home improvements, the interest may be tax-deductible under IRS rules. If the funds are used for personal expenses (e.g., debt consolidation), the interest is generally not deductible. Always consult a tax professional to understand how a cash-out refinance affects your specific tax situation.

Reviewed by: Bryan Dornan, HELOC Expert (25+ years) | Updated: June 2026 | Fact-Checked ✓

About Bryan Dornan

Bryan Dornan is a financial journalist and mortgage industry veteran with nearly 30 years of experience as a lender, loan officer, mortgage broker, and chief marketing officer. He currently serves as Chief Editor of RefiGuide.org, where he has built one of the most trusted mortgage education platforms in the United States. Bryan has founded multiple mortgage and digital marketing companies throughout his career and remains focused on helping homeowners leverage home equity wisely while making affordable homeownership accessible to everyday Americans. He is a licensed California Real Estate Broker DRE: #01203791. and writes for RealtyTimes, Patch, Buzzfeed, Medium and other national publications. Find him on Twitter, Muckrack, and Linkedin

More articles by Bryan Dornan