What Credit Score Do I Need for a HELOC?

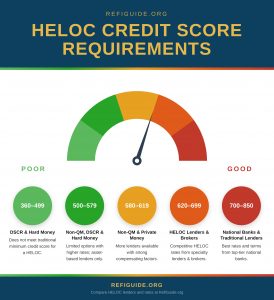

Most traditional banks and credit unions set a 620 FICO floor for a HELOC, but standard approval starts at 660–680. Scores of 740 and above earn the lowest rates and highest credit limits.

- Excellent Tier (Best Rates)

- 740+ FICO — lowest margin over prime, highest credit limits

- Standard Approval Tier

- 660–680 FICO — routine approval, mid-range pricing

- Traditional Minimum Floor

- 620 FICO — approval possible, higher rate and reduced limit

- Alternative Subprime / Non-QM Floor

- 500–620 FICO — Non-QM and hard money lenders only, substantially higher cost

Compensating factors — low CLTV, strong reserves, high income — can offset a borderline score.

In 2026, banks and home equity lenders continue to value stability and responsible credit behavior, specific HELOC credit requirements and eligibility factors shape who qualifies and on what terms. Understanding this lending criteria can improve your chances of approval and help you qualify more favorable HELOC rates and borrowing power. The RefiGuide published this article to illustrate how to improve your credit score so you can qualify for a competitive HELOC line of credit that best meet your needs. We updated the current HELOC credit score requirements and how they impact your home equity line of credit application, based on our lender surveys.

What Is the Minimum Credit Score for HELOC in 2026?

In most cases, the required credit-scores for a home equity line of credit in 2026 are 620 at most traditional banks and credit unions, but that floor only gets you in the door. Borrowers at 660–680 qualify for standard approval, while 700–720+ unlocks meaningfully lower rates. At 740 and above, you’ll access the most competitive terms and highest credit limits available. Lenders treat a HELOC as a second-lien loan — meaning they carry more risk than a first mortgage — so credit standards are enforced strictly. Compensating factors like low LTV, strong income, and substantial equity can sometimes offset a borderline score below 660.

However, if you have lower credit, alternative financing options are available. Non-QM lenders may approve borrowers with credit scores as low as 620, especially if there are compensating factors like low loan-to-value (LTV), high cash reserves, or strong rental income. These HELOC loans may have slightly higher interest rates and fees due to increased risk.

For those with poor credit (below 600), hard money lenders may offer HELOC-solutions or equity-based credit lines. These typically rely more on the property’s value than the borrower’s credit score, often allowing credit scores as low as 500 or even no score at all. However, interest rates are significantly higher, and terms are short—often 1 to 3 years.

Choosing the right HELOC option depends on your credit score, equity, and financial goals. Always compare lenders to find the best fit. Potential borrowers are always asking us how much of a HELOC line amount they can get with their credit scores. Since a HELOC is a second mortgage, the credit score is very important to the bank or mortgage lender.

Home equity line of credit (HELOC) loans allow you to use the equity in your home for cash. A minimum HELOC credit score is required with all traditional banks and lenders. It’s a secure loan where your home is the collateral. You can borrow money against the property based on your equity percentage.

However, the approval and the amount also depend on your credit score, among several other factors. In this article, you’ll learn about the minimum credit score for HELOCs. Let’s explore the possibility of getting a HELOC with bad credit scores as well. In this article, I will explain the details of how a HELOC works and the typical credit requirements you must meet to get approved for a home equity line of credit with a competitive rate.

Before we talk about the minimum HELOC credit score, it’s worth discussing why it’s a requirement in the first place. You may wonder why a credit score is necessary when your home’s equity is the basis of the line of credit.

The thing is that having a solid credit rating makes it easier for lenders to let you borrow money. Like other scenarios in which your creditworthiness plays a role, bad credit HELOC lenders also use your credit score to secure their interest.

A good credit score shows them that you’ll pay your dues on time and would likely not default. But your credit score’s importance doesn’t end there – it also helps determine the rate and terms. Generally, the higher the Fico-score you have, the easier it becomes to get the best available interest rates on the HELOC.

Again, it’s all about your creditworthiness– a higher credit score makes lending you money less risky, allowing lenders to give you a lower rate and higher HELOC credit limit.

HELOC Credit Score Data: What the Numbers Actually Show

The reality of who gets HELOCs today reveals a market where lenders set a far higher bar than most borrowers expect. Here is what the data shows:

- Average FICO score for HELOC borrowers is 771, up from 760 the prior year — well above the stated 620–680 minimums most lenders advertise (MBA 2025 Home Equity Lending Study, covering 2024 data)

- Average FICO score for home equity loan borrowers is 749, up from 742 (MBA 2025 Home Equity Lending Study)

- Average CLTV on funded HELOCs at closing fell to 51% from 53% — approved borrowers are not stretching to the limit, they are borrowing well inside it.

- Borrowers with scores above 760 hold approximately two-thirds of all tappable U.S. home equity (TransUnion / The Financial Brand)

- Home equity originations rose 16% year-over-year in Q1 2026, yet 85 million homeowners held an average of $277,000 in tappable equity — demand is still a fraction of available supply (TransUnion Q1 2026) Clayton

- Total tappable equity reached $21.6 trillion in Q1 2026 (TransUnion); ICE Mortgage Monitor’s narrower measure puts the figure near $11 trillion

- HELOC originations hit 352,000 in Q3 2025, up 15.8% year-over-year and the sixth consecutive quarterly gain, with Gen X and Baby Boomers the largest borrower segments at 38% and 30% TransUnion

- Total HELOC and home equity loan debt outstanding grew 10.3% in 2024, with lenders projecting 9.8% HELOC growth in 2025 and 9.5% in 2026 (MBA)

- A 1% rate difference on a $50,000 HELOC costs roughly $5,200 in extra interest over 15 years — at today’s pricing that is 7.43% versus 8.43%, or $33,074 against $38,258 in lifetime interest, making the gap between a 620 and a 740 score materially expensive

- The average HELOC credit limit reached $129,000 in March 2026, up from $123,000 a year earlier (Experian) Experian

- Debt consolidation accounted for roughly 39% of HELOC and home equity volume in 2024, up from 25% two years prior, while home renovation fell to 46% from 65% (MBA)

What Are HELOC Credit Requirements Today?

After surveying some of the top HELOC lenders in the country, I discovered that the minimum credit score for HELOC is 680 with most banks and conventional mortgage lenders. That said, you’re likely to get an easy and quick approval if your credit score is 700+.

Some HELOC lenders may lend money in a home equity line of credit to individuals with a credit score of 620 or above. However, in such cases, you can expect a relatively higher rate.

Also, the requirement typically does not allow for wiggle room, which means the minimum score is necessary even for initiating the process. If you have a lower credit score, you still may be able to qualify for a HELOC with bad credit. We will help you find private lenders that offer HELOCs with 500 credit scores if you need that.

If your fico score isn’t where you’d like it to be, consider improving it before applying for a new HELOC or home equity loan. Begin by obtaining a free credit report to assess your current standing. Review your credit rating and dispute any errors, late payments, collections or unauthorized charges to have them removed.

Does a HELOC Impact Credit? – Yes a HELOC can impact your credit in several ways, both positively and negatively, depending on how it’s managed. When you apply for a HELOC, the lender performs a hard inquiry on your credit report, which may temporarily lower your credit score by a few points. Once approved, the HELOC is reported as a revolving credit account, similar to a credit card, and becomes part of your credit profile.

The amount of the home equity line of credit and how you utilize it affect your credit utilization ratio, a key factor in your credit score. Keeping your balance low relative to the HELOC limit can positively impact your credit score by demonstrating responsible credit usage. Conversely, maxing out your HELOC or carrying a high balance can increase your utilization ratio, potentially lowering your score.

Timely payments are critical, as payment history is the most significant factor in determining your credit score. Consistently making on-time payments can strengthen your credit profile, while missed or late payments can harm it significantly. Additionally, the HELOC’s age contributes to your credit history, with longer credit accounts positively influencing your score.

Can You Get a HELOC with Low Credit Scores?

Understanding these criteria can improve your chances of approval—and help you secure more favorable rates and borrowing power. Although most second mortgage lenders set a minimum credit requirement for a home equity line of credit, some may consider applicants for a HELOC with a bad credit score or a no-credit history, provided they meet other HELOC requirements well above the minimum.

Taking out a HELOC with bad credit is possible if you meet the bank and lender’s HELOC requirements and guidelines. Understanding the various HELOC credit requirements can help you assess your eligibility. In addition to your credit score, the loan amount debt to income ratio, and appraised value will all be closely scrutinized.

The minimum credit score for a HELOC loan ranges from 640 to 700 in most banks. However, the minimum credit score for Non QM and private money lenders ranges from 550 to 620. There are hard money lenders extending high risk low credit HELOC loans for borrowers with credit scores as low as 500.

How Much HELOC Can You Qualify for Based on Your Credit Score?

You can calculate a home equity line of credit using a calculator online.

Most HELOC lenders will offer a basic calculator to estimate how much you’ll be able to borrow (if at all).

Again, your credit isn’t the only thing determining your eligibility and the sum you can borrow over a period.

That said, your credit score, current home value, and outstanding mortgage balance are enough for a rough idea before you begin the application.

How Does HELOC Affect Your Credit Score?

A HELOC application requires a hard credit pull, which can temporarily affect your credit ratings. So, it’s important to be absolutely certain and do your homework about the lender and the requirements before you apply.

Once your HELOC has been approved, its impact on your credit report is like any other debt. It depends on how well you manage it. Unlike a mortgage or home equity loan, it’s reported like a revolving credit. If you pay the HELOC payments on time, you can use it to improve your credit score.

Similarly, if you use the cash from HELOC to pay off other debts, you may see improvements in your credit. Closing a HELOC also impacts your credit history, especially if you don’t have other credit available. Essentially, if you have a big debt balance, you can expect a hit on your credit score.

Improving Your Credit Score for HELOC

If you have a lower credit score and want to apply for a HELOC with bad credit, you can work to improve your credit rating. Of course, that will take some time, but it’s entirely possible. You can build good credit with sound financial management and raise your credit scores to the minimum requirement set by the lender.

Here’s how you can do that:

Check Your Credit Report

It’s not uncommon for faulty items in your credit report to lower your credit scores. Credit reporting companies offer free annual credit reports. Look for any reporting errors from the credit bureaus, such as fraudulent accounts or wrong payments. You can request that such records be removed, which will improve your credit score.

Pay Debts and Avoid Late Payments

Paying your debit will work in your favor and improve your chances of getting HELOC approval in two ways. It will improve your credit score and bring down your DTI. More importantly, avoid late payments on your bills, as those directly impact your credit. Ensure you’re paying the minimum monthly amounts on your credit cards.

Key Points on HELOCs and Credit Scores

The HELOC credit score requirement is an important one, but not the only one. While you need credit scores of 680 or higher, you may still be able to get one if other requirements are met. That said, your chances are smaller if you have a low credit score and a bad credit history and may not get favorable conditions.

Besides your credit score, how much you owe on your home (and other loans) also plays a big role. So, even with a good credit score, a high DTI will negatively impact your application.

- Maximize HELOC funds for Cash Out

- Low HELOC Payments

- Find the Best HELOC Interest Rates

The RefiGuide can help you uncover the best home equity loans and HELOCs that are available with your specific fico number. You can shop with multiple lenders and brokers that will outline the current minimum HELOC credit score requirements so you can know what is available and if you meet the HELOC guidelines for the amount you want to borrow and the best possible HELOC interest rate.

Reviewing your credit scores and reports can provide insight into your standing and potential options. In many cases, you can check your FICO credit score for free through your bank, credit union, or Experian (one of the three major credit bureaus: Equifax, Trans Union and Experian). Additionally, third-party paid services may offer more detailed score tracking so you can meet you goals and the minimum credit score requirements for a HELOC.

Frequently Asked HELOC Credit Questions

What Credit Score Is Needed for a HELOC?

To qualify for a HELOC, most traditional lenders typically require a credit score of at least 620. However, if you have a 700 credit score or higher you may receive better interest rates and more favorable terms, such as lower interest rates and better borrowing limits. Some lenders may accept applicants with scores in the 600–620 range, but they often impose stricter terms like higher HELOC interest rates or reduced credit limits. Additionally, credit history, debt-to-income ratio (DTI) , and the amount of home equity you have also play critical roles in eligibility.

If your credit score falls below 620, alternative lending options may still be available, though they tend to carry steeper borrowing costs. To improve your chances of approval, consider paying down existing debt to lower your DTI ratio and ensuring that your credit report is free of errors. Shopping around with multiple lenders can also help you find more lenient credit requirements or promotional offers tailored for your financial profile.

Can I get a HELOC with a 600-credit score?

Most lenders require at least a credit score of 680 for HELOC. If you have 600 fico score, you may still be able to qualify, but you may need to do so at a higher rate. There are even a few lenders that offer a bad credit HELOC option for borrowers with credit scores between 500 and 600. Of course you will need more equity and a lower loan to value (LTV) to qualify for a HELOC with low credit scores.

Other requirements, such as the CLTV and DTI, may help you satisfy the lender for HELOC. If you do not qualify for a HELOC loan because your fico scores are too low, consider refinancing. See the current refinance mortgage credit score requirements.

Can I qualify a HELOC with 500 to 580 credit score?

Getting approved for a HELOC with a credit score between 500 and 580 can be challenging, as most traditional lenders prefer scores of at least 600. However, some specialized HELOC lenders or credit unions may offer HELOCs to borrowers with lower credit scores, though they typically impose higher interest rates, stricter repayment terms, and reduced borrowing limits. To improve your chances of approval, you might consider boosting your credit score by paying down outstanding debt and addressing any errors on your credit report. Exploring alternative lending, such as hard money non-QM loan, could also provide access to a home equity line of credit, though at a higher cost. It’s crucial to shop around and compare terms to ensure you get the best deal available for your credit profile.

How Does Your Credit Score Affect the Interest Rate on a HELOC?

Your credit score directly determines the margin lenders add above the prime rate on your HELOC. In practical terms: borrowers with scores 740+ typically receive the lowest available margin, often prime + 0%–0.5%. Scores in the 680–739 range usually add 0.5%–1.5% to the base rate. Scores of 620–679 may carry margins of 1.5%–3.0% above prime. On a $100,000 HELOC, a 1% rate difference equals $1,000 per year in additional interest. Even raising your score 20–40 points before applying can meaningfully reduce your lifetime borrowing cost.

Does Applying for a HELOC Hurt Your Credit Score?

Yes — but minimally and temporarily. A HELOC application triggers a hard credit inquiry, which typically causes a 5–10 point dip in your score. However, when shopping multiple HELOC lenders within a 14–45 day window, credit bureaus often treat all inquiries as a single pull for scoring purposes — so rate shopping does not compound the impact. Long-term, a well-managed HELOC can actually improve your credit by diversifying your credit mix and lowering overall utilization if you consolidate revolving debt. Avoid opening new credit accounts or making large purchases during the 30–60 days before applying.

Can Adding a Co-Borrower Help You Qualify for a HELOC With a Low Credit Score?

Yes — adding a co-borrower or joint applicant with a stronger credit profile can significantly improve HELOC approval odds when your own score falls short. Most lenders use the lower of the two borrowers’ middle credit scores as the qualifying score, so the co-borrower’s credit strength only helps if their score is higher than yours AND lender guidelines allow the stronger score to control pricing. Some lenders instead use the primary borrower’s score; always confirm the lender’s policy before applying. The co-borrower’s income also counts toward DTI qualification, which can expand your borrowing capacity beyond what you could access individually.

What Are the Fastest Ways to Improve Your Credit Score Before Applying for a HELOC?

The fastest credit score improvements before a HELOC application come from: (1) paying down credit card balances to below 30% utilization — which can boost scores in one to two billing cycles; (2) disputing errors on your credit report at AnnualCreditReport.com — corrected errors can lift scores within 30–45 days; (3) becoming an authorized user on a long-standing account with low utilization; and (4) avoiding new credit applications for at least 60 days before applying. Late payments have the largest negative impact and take longer to recover from — consistent on-time payments are essential for rebuilding a damaged score.

Do you need good credit for the best HELOC interest rate?

Yes, good credit (typically 700+, ideally 740+) is essential for a low-rate HELOC in 2026. Lenders like LoanDepot and Bank of America offer rates as low as 6.99% APR for high credit scores, while scores below 620 may face rates above 9%. A strong credit score and low debt-to-income ratio (below 43%) secure better terms.

Does an unused HELOC affect credit score?

An unused HELOC may slightly lower your credit score due to the new credit inquiry and increased available credit affecting utilization ratios. However, the impact is minimal if you maintain low debt levels elsewhere. Lenders like PNC report unused HELOCs to credit bureaus, but responsible management prevents negative effects.

Can you get a HELOC with collections or charge-offs on your credit?

HELOC approval with collections or charge-offs is possible but challenging, requiring compensating factors like substantial equity (30%+), low debt-to-income ratio (below 36%), and strong recent payment history. Most lenders require collections and charge-offs to be paid or settled before closing, particularly if recent (within 12-24 months) or exceeding $2,000-5,000. Older collections (3+ years) may be overlooked if you demonstrate 12-24 months of perfect payment history since the derogatory mark. However, unpaid tax liens or judgments typically result in automatic denial. Expect higher interest rates (1-2% premium) and lower credit limits (65-70% CLTV versus 80-85% standard) with derogatory marks on credit.

What happens to your HELOC if your credit score drops after approval?

After HELOC approval, lenders cannot change your interest rate, credit limit, or terms based solely on credit score drops, but they can freeze or reduce your credit line if you miss payments, exceed debt limits, or if home values decline significantly. Most HELOCs include adverse action clauses allowing lenders to suspend borrowing privileges during draw period if credit score drops below 620-640, you become 60+ days late on any debt, file bankruptcy, or combined loan-to-value exceeds 80-85% due to property value decline. However, amounts already borrowed remain accessible at original terms. Your interest rate continues adjusting based on prime rate, not credit score—rate increases reflect market conditions, not personal creditworthiness. To protect HELOC access: maintain 620+ credit score, keep all payments current, monitor home values, and avoid maxing out credit line. If line is frozen, demonstrating 6-12 months improved payment history may restore borrowing privileges.

Does a HELOC Affect Your Credit Utilization Ratio?

A HELOC affects credit utilization differently than a credit card. Because it is a secured revolving line, most credit scoring models treat it separately from unsecured revolving credit — meaning it typically does not factor into the standard credit utilization ratio that affects your FICO score the same way a Visa or Mastercard balance does. However, carrying a large balance near your HELOC limit can signal risk to some lenders during manual underwriting review. Keep your drawn balance below 30% of the approved HELOC limit to maintain the strongest credit profile.

What Documents Are Required to Obtain a HELOC in 2026?

Most HELOC lenders require: two years of W-2s or federal tax returns, 30 days of recent pay stubs, two months of bank and asset statements, your most recent mortgage statement showing current balance and payment history, a homeowners insurance declarations page, and a government-issued photo ID. Self-employed borrowers additionally need two years of business returns and a current P&L statement. Review best HELOC lenders in 2026 to compare which lenders offer streamlined document requirements and digital application processes.

Do HELOCs Show Up on Your Credit Report?

Yes — a HELOC appears on your credit report in two stages. First, the lender pulls a hard inquiry when you apply, typically reducing your FICO score by 3–5 points temporarily. Once approved and opened, the HELOC appears as a revolving credit account on all three bureaus — Equifax, Experian, and TransUnion — showing your credit limit, current balance, and payment history. On-time HELOC payments reported monthly build positive payment history over time. A HELOC is never invisible to creditors; always factor it into your overall credit profile before applying for other financing.

Which credit score do HELOC lenders actually use?

Most HELOC lenders pull a tri-merge report and rely on classic FICO mortgage versions — FICO 2, 5, and 4 from Experian, Equifax, and TransUnion — then qualify you on the middle of those three scores. Joint applications typically use the weaker borrower’s middle score. This matters because the free VantageScore 3.0 shown in Credit Karma or your banking app often runs 20 to 60 points higher than your mortgage FICO. Pull your actual mortgage scores before assuming you clear a 680 threshold.

Do HELOC lenders check your credit again before closing?

Yes. Nearly all lenders run a soft refresh or full re-pull within days of closing, along with an undisclosed debt monitoring report that flags any new inquiry or account opened during underwriting. Financing a car, opening a store card, or running up balances after approval can raise your DTI, trigger re-underwriting, or shrink your approved line. Keep new credit on hold until funding — it also prevents avoidable delays in the HELOC-approval timeline.

Does Getting a HELOC Require You to Refinance Your Existing Mortgage?

No — a HELOC does not require you to refinance your existing mortgage. It is a completely separate second-lien loan that sits behind your first mortgage without altering its rate, term, or payment in any way. This is one of the most significant advantages of a HELOC over a cash-out refinance for homeowners holding low first mortgage rates from 2020–2022. For a detailed comparison of when a HELOC makes more financial sense than refinancing, the HELOC vs. home equity loan guide provides a full cost analysis.

What Are Current HELOC Rates for Excellent Credit in 2026?

Borrowers with 740+ FICO scores and 80% or lower CLTV are accessing the most competitive HELOC rates available — currently ranging from 6.25%–7.00% APR at the best-pricing lenders as of May 2026, compared to the national average of 7.17% APR, according to Bankrate, May, 2026. Excellent credit borrowers also qualify for the highest available credit limits and most favorable draw terms. To compare current offers across lenders by credit tier, review today’s HELOC rates with verified lender data updated monthly.

What Is the DTI Requirement for a HELOC in 2026?

Most HELOC lenders require a maximum debt-to-income (DTI) ratio of 43%, calculated by dividing all monthly debt payments — including your mortgage, the estimated new HELOC payment, car loans, student loans, and credit card minimums — by gross monthly income. Some lenders accept up to 50% DTI for borrowers with strong compensating factors like excellent credit scores or substantial equity. A few stricter lenders cap at 36%. Borrowers near the limit can lower their DTI by paying down revolving debt before applying, or by adding a co-borrower with additional income to the application.

How Much Equity and What CLTV Do You Need to Qualify for a HELOC?

Most HELOC lenders require homeowners to retain at least 15%–20% equity after the credit line is established, meaning the combined loan-to-value (CLTV) — your primary mortgage balance plus the HELOC — typically cannot exceed 80%–85% of your home’s appraised value. Example: on a $400,000 home, an 85% CLTV cap means total secured debt cannot exceed $340,000. If you owe $220,000 on your mortgage, the maximum HELOC would be $120,000. Borrowers with lower credit scores generally face stricter CLTV caps, sometimes limited to 75%–80%, requiring more equity to qualify for the same loan amount.

What Income Documentation Is Required for a HELOC Application?

HELOC income documentation varies by employment type. W-2 employees typically provide recent pay stubs, two years of W-2s, and federal tax returns. Self-employed or 1099 borrowers must usually provide two years of personal and business tax returns, a recent profit-and-loss statement, and sometimes bank statements. Retirees document income via Social Security award letters, pension statements, or IRA/investment distribution records. Rental income is typically documented via Schedule E and current lease agreements, with lenders counting 75% of gross rental income toward qualifying income. No-doc HELOC programs exist for borrowers who cannot verify income through traditional means but require stronger equity and credit.

Much like a mortgage, you should consider refinancing a home equity loan if your current lender is offering you poor conditions like a high interest rate or not enough money. Many traditional banks and lenders do not offer home equity lines of credit, so you may need a 2nd mortgage lender to refinance a HELOC. It also depends on whether another lender or bank is willing to offer you HELOC refinancing. You’ll need to apply for a new HELOC with the new lender and begin refinancing.

What are the closing costs on a HELOC or home equity loan?

Most mortgage lenders will charge closing costs on home equity loans and HELOCs. The lending fees and closing costs range from 1 to 5% in most cases. You can expect most banks and credit unions to charge an annual fee for HELOCs, but most lenders will waive that fee.

Summary on HELOC Credit Requirements

The RefiGuide can help you learn about the current HELOC requirements and connect you with experienced home equity lenders that offer competitive interest rates on HELOCs, home equity loans and cash-out refinances. A HELOC functions much like a credit card, providing you with credit that’s available when you need it. Getting a HELOC for bad credit can be challenging but is possible if you have strong credentials like a low debt to income ratio and a low loan to value ratio. However, qualifying for these loans can be challenging, as they often require a significant amount of home equity and a high credit score.

Reviewed by: Bryan Dornan, Lending Expert (25+ years) | Fact Checked ✓

Disclosure: RefiGuide.org is an advertising marketplace, not a licensed mortgage lender or broker. Loans are matched with participating NMLS-licensed institutions.

About Bryan Dornan

Bryan Dornan is a financial journalist and mortgage industry veteran with nearly 30 years of experience as a lender, loan officer, mortgage broker, and chief marketing officer. He currently serves as Chief Editor of RefiGuide.org, where he has built one of the most trusted mortgage education platforms in the United States. Bryan has founded multiple mortgage and digital marketing companies throughout his career and remains focused on helping homeowners leverage home equity wisely while making affordable homeownership accessible to everyday Americans. He is a licensed California Real Estate Broker DRE: #01203791. and writes for RealtyTimes, Patch, Buzzfeed, Medium and other national publications. Find him on Twitter, Muckrack, and Linkedin

More articles by Bryan Dornan